Just because a stock looks cheap doesn’t necessarily mean it’s a bargain.

Some stocks look undervalued, but that’s because they’re actually poor businesses that are destined to fail.

These stocks are called value traps because they can draw value investors in, but they end up being a trap.

This article covers five major red flags that you can use to help you avoid value traps.

1. Declining or Negative Revenue Growth

One of the biggest red flags in a stock that looks cheap is that the company is seeing stagnant or declining revenue.

Even if a stock has a low valuation, its stock price might struggle to rise if its top-line growth is deteriorating.

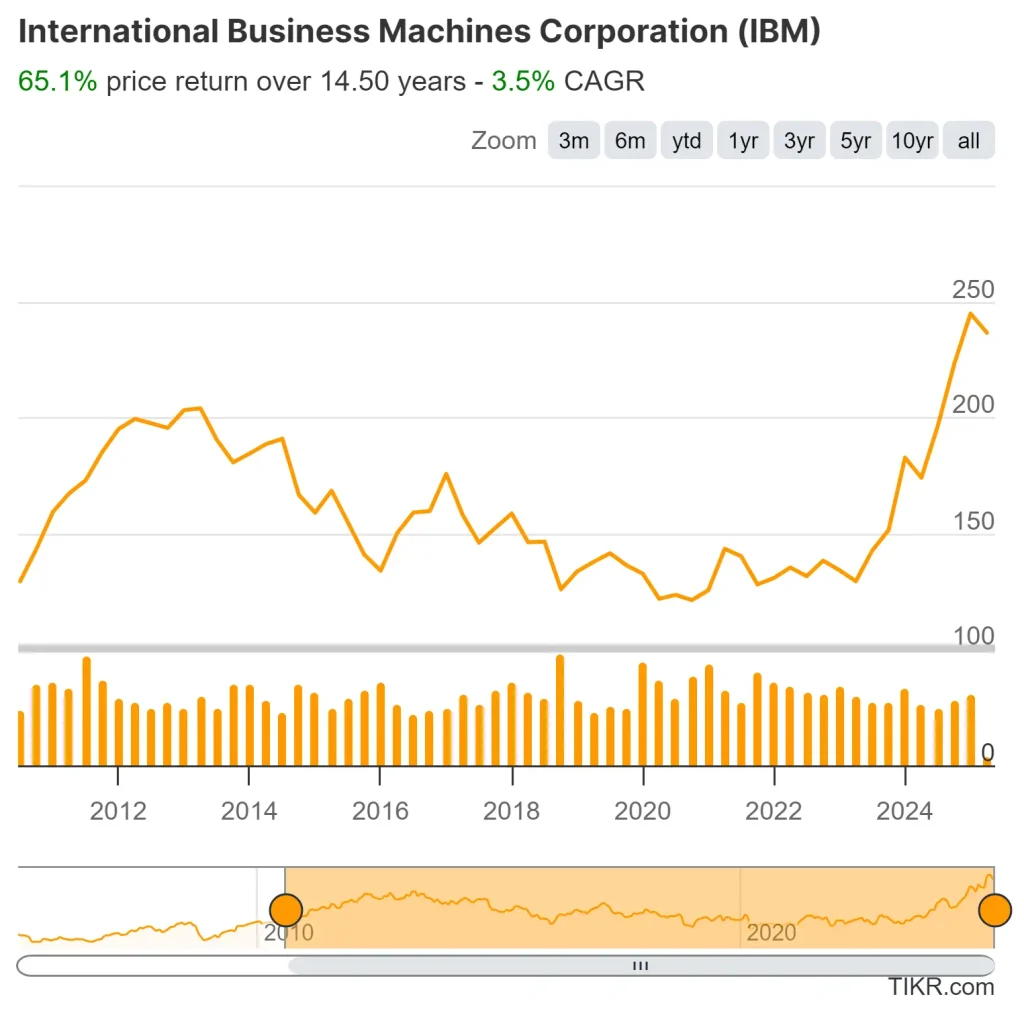

Example: IBM (IBM)

- For years, IBM appeared undervalued based on its P/E ratio and dividend yield.

- However, from 2012 to 2020, IBM’s revenue consistently declined as it struggled to transition from legacy hardware to cloud computing.

- Despite multiple turnaround efforts, IBM’s stock remained flat while competitors like Microsoft (MSFT) surged due to strong revenue growth.

2. Weak Earnings Quality & Aggressive Accounting

A company may report strong earnings, but if those profits rely on one-time gains, accounting tricks, or non-core activities, the business may not be as healthy as it seems.

Why It Matters

Some companies manipulate earnings through:

- One-time asset sales: Selling a division to create a temporary boost in profits.

- Overly aggressive revenue recognition: Booking sales before they are truly earned.

- Non-operating income: If a significant portion of earnings comes from non-operating income, it may be unsustainable.

Investors should look beyond headline earnings and examine whether profits come from sustainable operations.

Example: General Electric (GE)

- For years, GE reported strong earnings, but much of its profits came from financial engineering rather than true business growth.

- In 2018, GE had to take massive write-downs after years of over-reported earnings, leading to a dividend cut and stock collapse.

- The company’s stock fell over 75% from its 2016 peak as investors realized the business had overstated earnings.

Analyze stocks quicker with TIKR >>>

3. High Debt and Unsustainable Dividend Yields

A high dividend yield may seem attractive, but if the dividend is being funded by debt or deteriorating cash flows, it may not be sustainable.

Why It Matters

High debt limits a company’s ability to invest in growth, weather downturns, or return capital to shareholders.

In extreme cases, high debt levels can force companies to cut dividends, dilute shareholders by issuing new shares, or even file for bankruptcy.

- Debt-to-Equity Ratio: A high ratio (above 2.0) can indicate that a company has excessive leverage, which may put dividends and growth at risk.

- Payout Ratio: If a company is paying out more than 100% of earnings in dividends, it may not be sustainable.

Example: Frontier Communications (FTR)

- Frontier once had a dividend yield above 10%, making it appear highly attractive to income investors.

- However, the company’s high debt load made the dividend unsustainable, and it eventually had to slash its payouts.

- Frontier’s stock collapsed by over 90% before eventually filing for bankruptcy in 2020.

Additional Example: AT&T (T)

- AT&T historically carried high debt, and in 2022, it cut its dividend by nearly 50% to help manage its balance sheet. Many were caught off guard by the payout reduction.

Investors can avoid the most common value trap signals by checking revenue trends, earnings quality, and financial leverage.

However, there are still more red flags to watch for, including declining competitive advantages and poor capital allocation.

Find the best high-quality stocks to buy with TIKR >>>

4. Declining Competitive Advantage (Eroding Moat)

A company that once had a strong market position can become a value trap if it loses its competitive advantage, or “moat.”

If a business can no longer defend its market share, it may struggle to grow earnings, leading to long-term underperformance.

Why It Matters

A company’s moat protects it from competitors and ensures pricing power, customer loyalty, and long-term profitability.

When a moat erodes due to technological disruption, stronger competitors, or shifting consumer preferences, the company might never regain its former strength.

- Market Share Trends: If a company is consistently losing market share to competitors, it may be a long-term decline rather than a temporary setback.

- R&D Spending: Companies with shrinking research and development budgets may be failing to innovate and remain competitive.

Example: Kodak (KODK)

- Kodak was once the dominant player in the photography industry and had a strong brand.

- However, it failed to adapt to digital photography, allowing competitors like Canon and Sony to take market share.

- The company’s slow reaction to industry changes led to its 2012 bankruptcy despite its stock looking “cheap” for years.

5. Management Issues and Poor Capital Allocation

Even a company with a strong brand and low valuation can become a value trap if management repeatedly makes poor decisions.

Whether it’s reckless spending, bad acquisitions, share buybacks at inflated prices, or excessive executive compensation, poor capital allocation can destroy shareholder value.

Key Metrics

- Insider Buying vs. Selling: If executives are selling large amounts of stock, it may signal a lack of confidence in the business.

- Return on Invested Capital (ROIC): A consistently low or negative ROIC indicates that the business isn’t creating shareholder value from its investments.

See what the world’s best investors are buying with TIKR >>>

Example: Sears (SHLD)

- Sears was once a retail powerhouse, but poor management decisions led to its downfall.

- CEO Eddie Lampert prioritized financial engineering over investing in stores and online operations.

- Instead of innovating, Sears cut costs aggressively, failed to modernize, and ultimately filed for bankruptcy.

Additional Example: Bed Bath & Beyond (BBBY)

- Management focused on stock buybacks instead of improving operations, which ended up depleting cash reserves without improving the business.

- The company’s lack of strategic direction led to a dramatic stock collapse in 2022 and 2023.

Tips to Avoid Value Traps

To avoid value traps, it’s important for investors to go beyond simple valuation metrics and analyze the full picture of a company’s financial health, competitive position, and management quality.

1. Use a Multi-Metric Approach

- Look for low valuation ratios (P/E, P/B, EV/EBITDA), but confirm that the company has stable/growing revenue and earnings.

- Check financial health metrics like debt levels, cash flow, and liquidity.

- Analyze competitive positioning to ensure the company still has a competitive advantage in its industry.

2. Compare to Industry Peers

- If a company looks cheap, check whether competitors are growing while it is shrinking.

- If an entire industry is struggling, the valuation may not recover soon.

3. Look for a Clear Growth Catalyst

- Cheap stocks need a reason to rise. Whether it’s a turnaround strategy, new leadership, or industry tailwinds, there should be a potential upside.

- Avoid companies without a clear strategy for reversing their decline.

Historical Example: Microsoft (MSFT) Turnaround

- In the early 2010s, Microsoft was considered a value trap as it struggled in mobile and cloud computing.

- However, under Satya Nadella’s leadership, Microsoft shifted its focus to cloud services, driving massive stock gains.

- This turnaround showed how strong leadership and capital allocation can rescue a struggling stock.

Avoiding value traps requires a comprehensive approach that goes beyond just looking at low valuation ratios.

Investors must verify financial stability, competitive position, and growth potential before considering whether a stock belongs in their portfolio.

FAQ Section:

What are the biggest red flags of a value trap?

The biggest red flags of a value trap include declining revenue, poor earnings quality, high debt, loss of competitive advantage, and weak management. Stocks that appear cheap but continue to underperform often have fundamental issues that prevent recovery.

How can you tell if a stock is a value trap or undervalued?

A stock is a value trap if it remains cheap due to fundamental problems, while a truly undervalued stock has strong financials and a clear path to recovery. Checking growth trends, debt levels, and competitive position can help distinguish the two.

Why do some undervalued stocks never recover?

Some undervalued stocks never recover because they lack earnings growth, face industry disruption, or have mismanaged leadership. Companies in declining industries, with excessive debt, or poor capital allocation often struggle indefinitely.

What metrics help investors spot if a stock is a value trap?

To avoid value traps, investors should not rely on a single metric. Important factors to check include:

- Revenue growth trends (Is the company shrinking?)

- Debt-to-equity ratio (Can the company manage its liabilities?)

- ROIC (Return on Invested Capital) (Is management allocating capital wisely?)

- Insider buying vs. selling (Are executives confident in the stock?)

What are some historical examples of value traps in the stock market?

Some value traps with stocks that have happened in the past include:

- Kodak (KODK): Failed to adapt to digital photography, leading to bankruptcy.

- Sears (SHLD): Focused on financial engineering instead of retail innovation, eventually collapsing.

- General Electric (GE): Used aggressive accounting to inflate earnings, leading to long-term underperformance.

- Frontier Communications (FTR): Had an unsustainable dividend due to excessive debt, leading to bankruptcy.

TIKR Takeaway:

Spotting value traps early can save you from costly mistakes.

By watching out for these red flags, you can focus on true bargains and avoid stocks that are cheap for the wrong reasons.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks, so if you’re looking to find the best stocks to buy for your portfolio, you’ll want to use TIKR!

TIKR offers institutional-quality research for investors who think of buying stocks as buying a piece of a business.

Sign up for free right now! >>>

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. We aim to provide informative and engaging analysis to help empower individuals to make their own investment decisions. Neither TIKR nor our authors hold any positions in the stocks mentioned in this article. Thank you for reading, and happy investing!