Valuing a stock doesn’t have to take hours of research or complex financial models.

This article outlines a quick valuation method that allows investors to value a stock in minutes, helping investors to filter through stock ideas faster.

This framework can help you easily estimate a stock’s fair value with surprising accuracy, but it doesn’t replace the value of doing detailed due diligence and research on a stock.

Table of Contents:

- The 3-Step Quick Valuation Method

- How to Verify Your Quick Valuation

- Limitations of Quick Valuations

- TIKR Takeaway

Let’s dive in!

The 3-Step Quick Valuation Method

Step 1: Estimate Normalized Earnings Per Share (EPS)

A company’s earnings per share (EPS) reflects how much profit the business generates for each share of stock. Investors can use normalized EPS, which adjusts EPS for one-time items and economic cycles, to get a clearer picture of a company’s future earnings power.

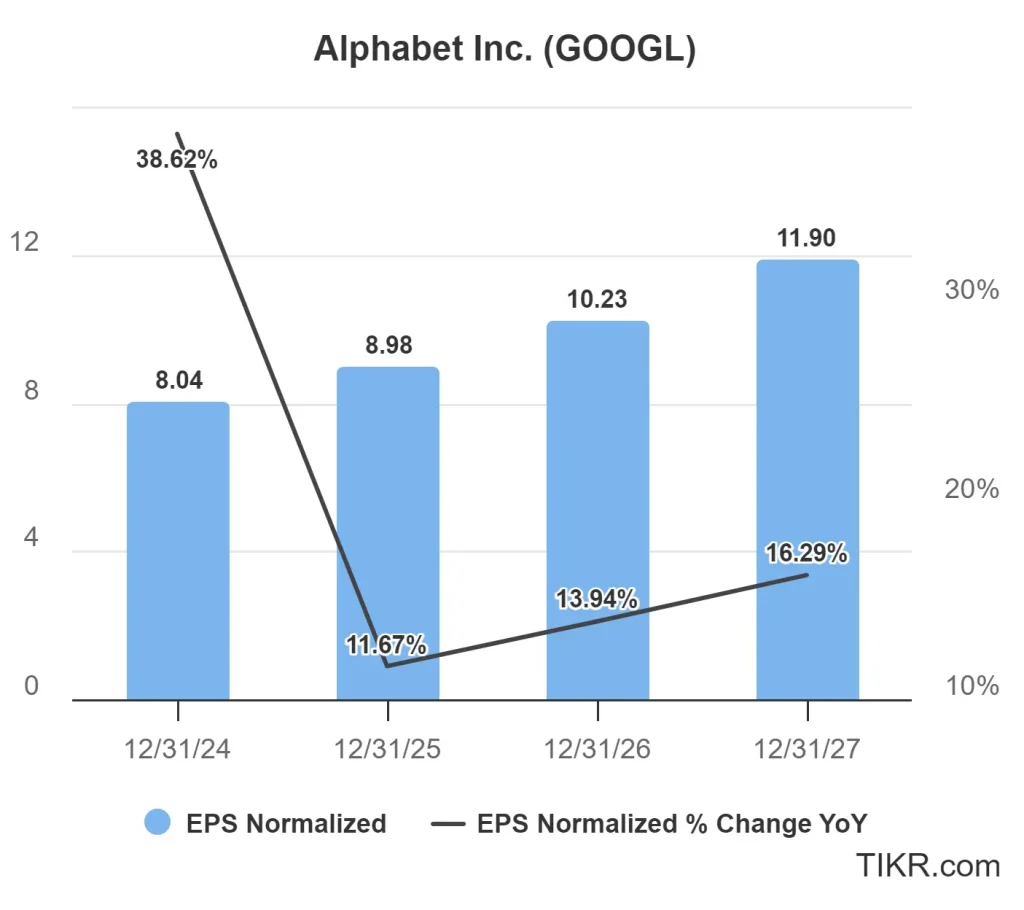

One way to estimate normalized EPS is by looking at analyst esimates. For example, Google (GOOGL) is expected to earn $11.90 per share 3 years from now.

Analyze stocks quicker with TIKR >>>

This number accounts for the average analyst earnings estimate across the dozens of analysts who cover Google. Investors can use reduced figures if they’d like to be more conservative in their valuation.

Investors should also adjust for business cycles. For cyclical industries like oil and gas, using average EPS over a full cycle provides a more reliable estimate.

If ExxonMobil (XOM) posts record earnings during an oil price boom, assuming those earnings will continue indefinitely can lead to an inflated valuation.

Step 2: Select a Reasonable P/E Multiple

The price-to-earnings (P/E) ratio tells investors how much the market is willing to pay for each dollar of earnings. Choosing the right P/E multiple depends on several factors:

- Historical averages: If a stock has historically traded at 20x earnings, using that as a benchmark makes sense.

- Industry comparisons: If a company operates in a sector where peers trade at 25x earnings, but it trades at 15x, it could be undervalued.

- Growth expectations: High-growth companies often command higher P/E ratios. A company growing earnings at 20% per year may trade at 30x earnings, while a slow-growing utility company trades at 10x.

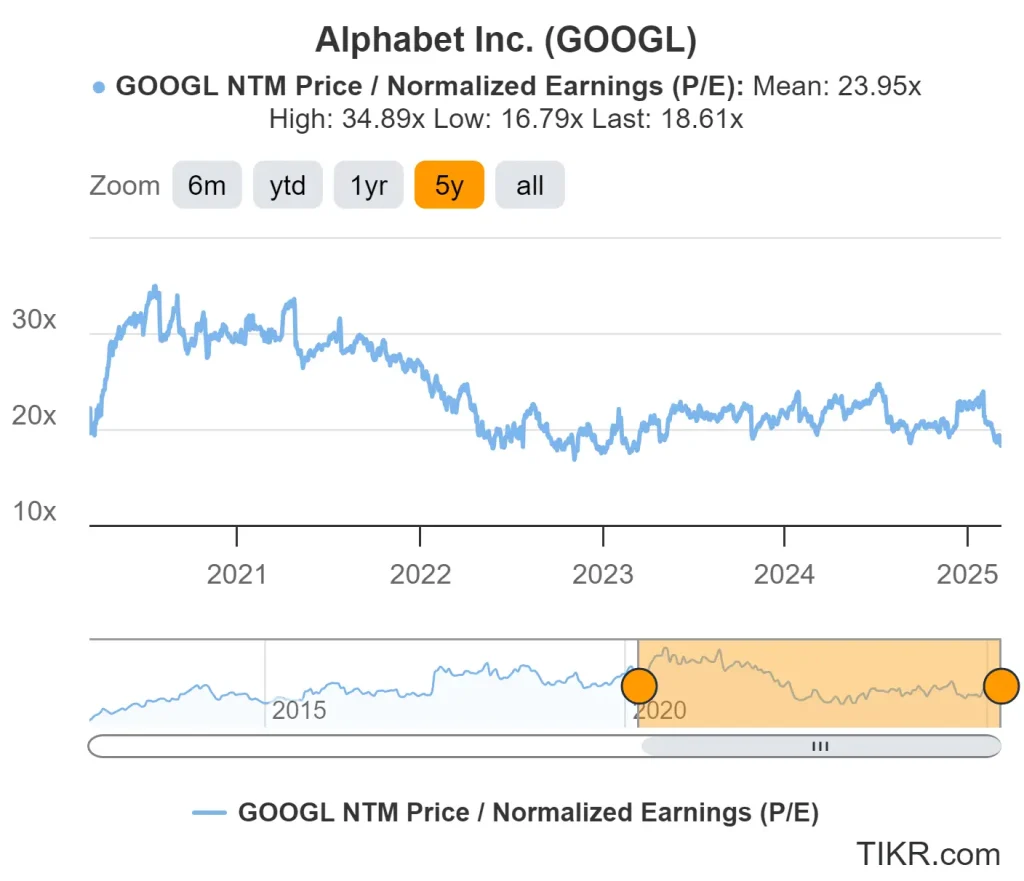

For example, over the past 5 years, Alphabet (GOOGL) has averaged a 24x P/E ratio. We can use a 20x P/E ratio to be a bit more conservative.

A reasonable P/E ratio depends on market conditions and expected growth. During bull markets, investors tend to pay higher multiples. During downturns, sentiment shifts, and stocks often trade at compressed valuations.

Additionally, stocks tend to pay at a P/E ratio that’s about 1 to 2 times their annual expected earnings growth. Since Google’s EPS is expected to grow at 14% annually, it’s very reasonable that the stock can trade at 20x earnings 2 years from now.

By selecting a realistic P/E multiple, investors can avoid overpaying for a stock while ensuring their valuation remains grounded in historical and industry trends.

Value stocks quicker with TIKR >>>

Step 3: Calculate the Stock’s Fair Value

Once investors have an estimate for normalized EPS and a reasonable P/E multiple, they can calculate a stock’s fair value using a simple formula:

Expected Normalized EPS × Forward P/E Ratio = Fair Value Estimate

For example, since Google’s expected earnings per share in three years is $11.90, applying a 20x forward P/E multiple gives us a fair value estimate of $238 per share.

$11.90 EPS × 20x P/E = $238 expected price per share

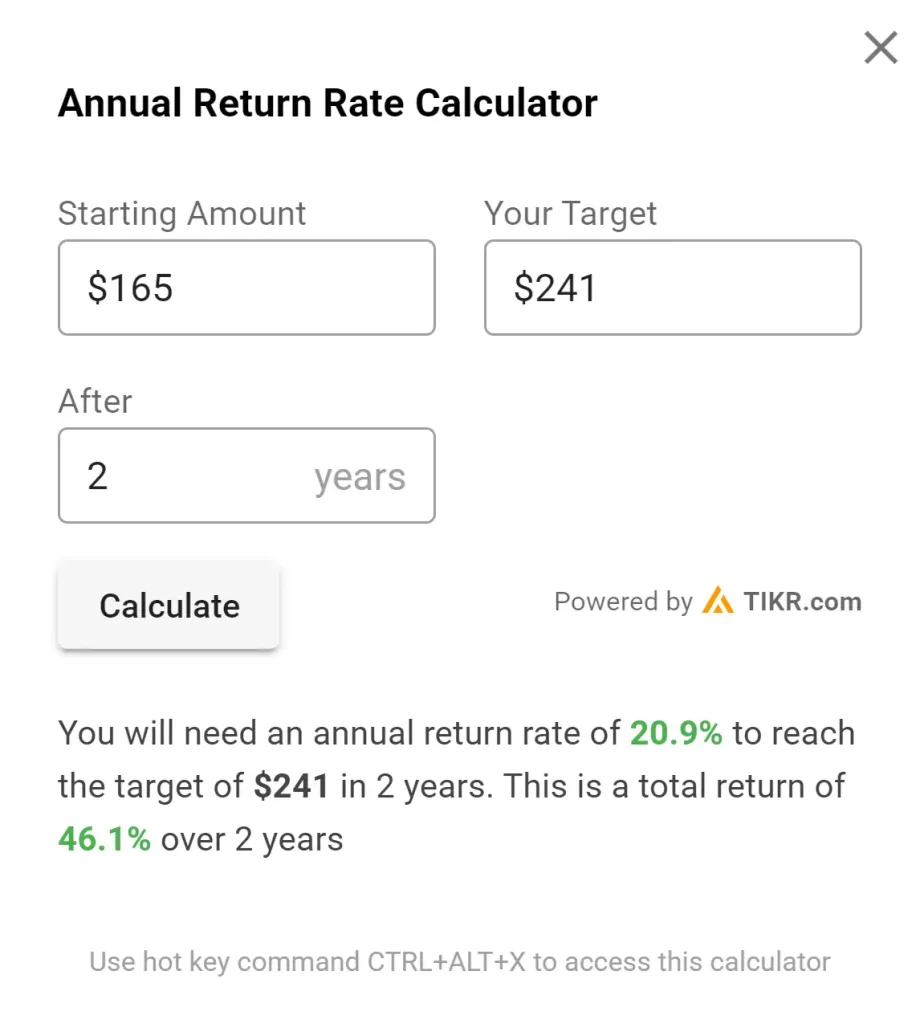

Additionally, the stock is expected to pay about $3/share in dividends over the next 3 years, which would bring the total expected fair value to $241/share.

Since Google trades at $165 today, this suggests a potential 46% upside over the next 2 years. We’re using a forward P/E multiple which values a stock based on its next 12 months expected earnings, which is why we think it would reach its $241 fair value in 2 years instead of 3.

How to Verify Your Quick Valuation

Here are some ways to cross-check your quick valuation.

Compare Against Analyst Price Targets

Analysts publish price targets based on detailed financial models. While these estimates are not perfect, they offer a benchmark.

If an investor’s valuation significantly differs from consensus targets, it may be worth reviewing assumptions.

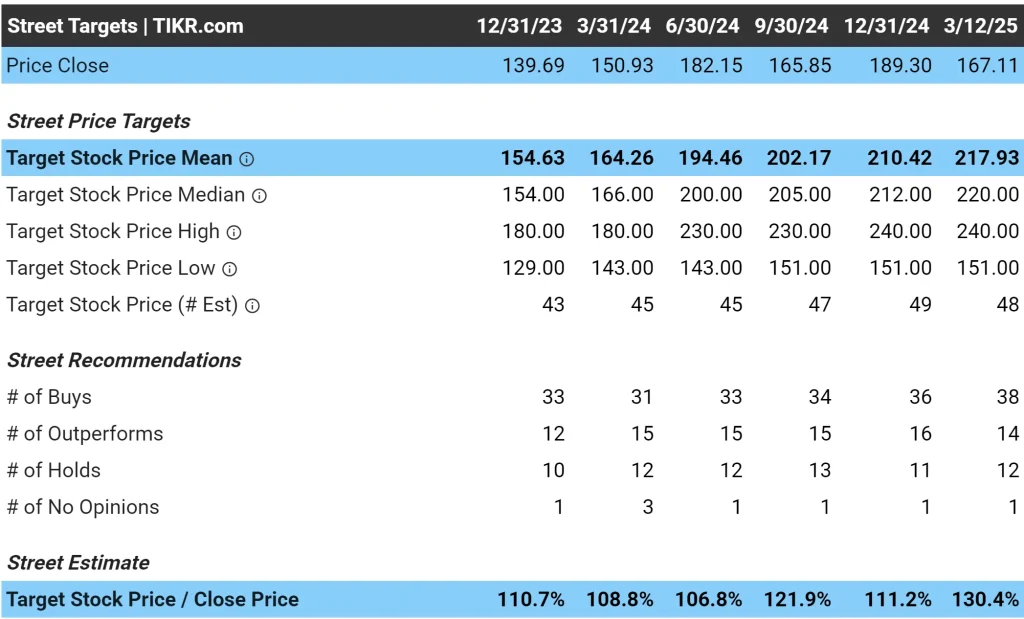

Analysts have a consensus price target for Google of about $218/share, which implies that they see about 30% upside today for the stock.

For reference, our fair value estimate for Google was about $241/share in 2 years. Either way, it looks like Google has a nice upside today.

Use Other Valuation Multiples

The P/E ratio is a useful metric, but it is not the only one. Investors can cross-check their valuation with:

- Price-to-sales (P/S) ratio – Useful for high-growth companies with lower earnings.

- Enterprise value to EBITDA (EV/EBITDA) – Helps compare companies with different capital structures.

- Discounted cash flow (DCF) model – More detailed, but useful for long-term investors.

Find the best stocks to buy today with TIKR >>>

Limitations of Quick Valuations

Quick valuations provide useful insights, but they have limitations.

Ignores Qualitative Factors

Numbers tell part of the story, but a company’s competitive advantage, management quality, and industry trends matter just as much.

A company with strong financials but a declining market position may not be a good investment.

For example, IBM appeared cheap on a P/E basis for years, but its declining relevance in enterprise software limited long-term returns.

Can Miss Cyclical Risks

Companies in cyclical industries experience earnings swings. A low P/E ratio may indicate that earnings are peaking rather than the company being undervalued.

Investors should adjust EPS estimates to reflect average earnings over a full cycle.

Requires Assumptions About the Future

Valuation depends on future earnings and market sentiment. If growth slows or investor sentiment changes, a stock’s fair value estimate may not hold.

FAQ Section

How do you quickly determine if a stock is undervalued?

Investors can compare a stock’s expected future earnings per share (EPS) multiplied by a reasonable price-to-earnings (P/E) ratio against its current price. If the estimated fair value is higher than the stock’s price today, it may be undervalued.

What is the fastest way to value a stock?

A simple method involves estimating a company’s future EPS, applying a reasonable P/E multiple, and calculating the expected share price. This provides a quick snapshot of whether a stock is trading above or below its fair value.

How do you find a reasonable P/E ratio for a stock?

A reasonable P/E ratio depends on the stock’s historical trading range, industry comparisons, and growth expectations. High-growth companies typically trade at higher P/E multiples, while mature, slower-growing businesses trade at lower ones.

Why is EPS important in stock valuation?

Earnings per share (EPS) represents a company’s profitability on a per-share basis. It is a key input in valuation models because it reflects how much profit the company generates for its shareholders.

Should quick valuations replace detailed research?

Quick valuations provide a useful starting point but should not replace deeper analysis. Investors should verify their estimates by considering other valuation methods, business fundamentals, and industry trends before making investment decisions.

TIKR Takeaway

Investors can quickly value a stock by estimating future EPS and multiplying by a reasonable P/E multiple.

This approach doesn’t replace thorough research, but it can help to filter opportunities and identify stocks worth further analysis.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks, so if you’re looking to find the best stocks to buy for your portfolio, you’ll want to use TIKR!

TIKR offers institutional-quality research for investors who think of buying stocks as buying a piece of a business.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. We aim to provide informative and engaging analysis to help empower individuals to make their own investment decisions. Neither TIKR nor our authors hold any positions in the stocks mentioned in this article. Thank you for reading, and happy investing!