Despite a weak consumer environment, analysts see a 62% upside for Celsius stock.

Celsius just reported Q2 earnings, where CEO John Fieldy noted that Celsius’s second-quarter sales were stunted by the “second quarter energy drink category slowdown.”

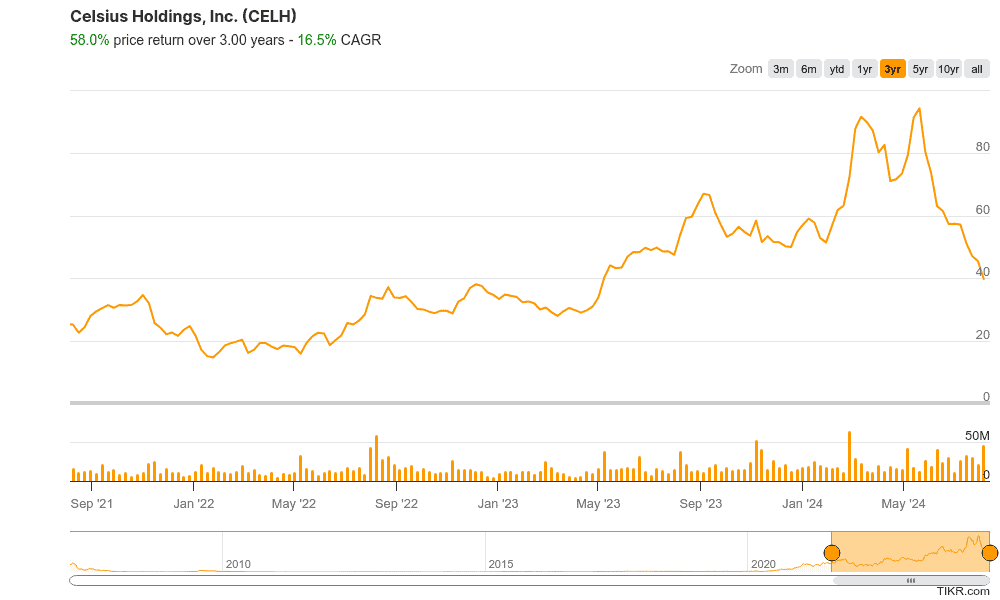

This and other factors have contributed to Celsius Holdings (CELH) stock seeing a 56.1% price drop in the past 3 months from about $87/share to $38/share today:

Celsius Holdings sells fun fitness drinks, mainly in the United States. You’ve probably seen Celsius’s drinks if you’re in the United States. If you haven’t, they come in various flavors like orange, wild berry, pineapple coconut, watermelon berry, and more.

What’s the outlook for Celsius Holdings?

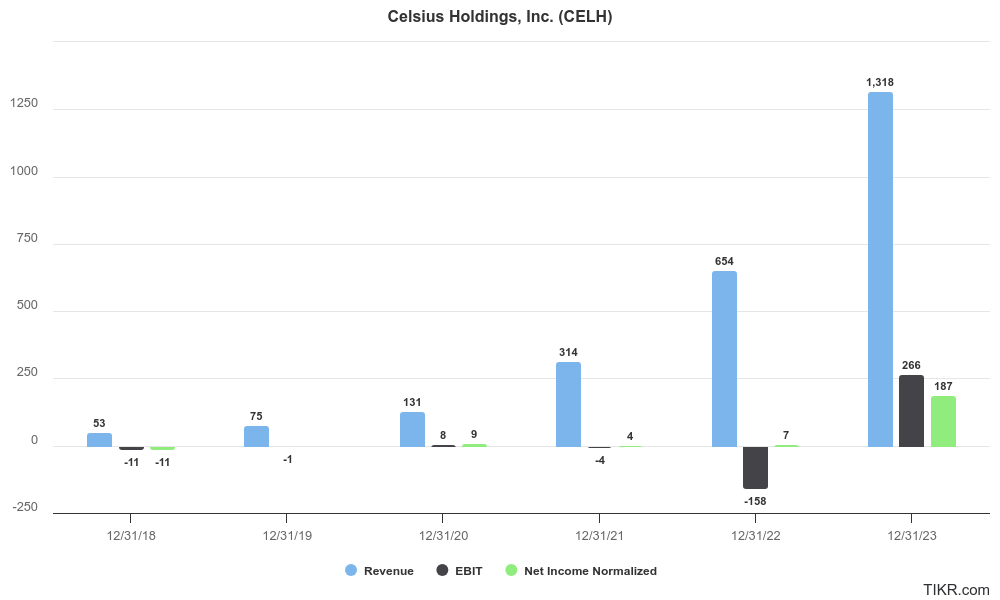

Over the past 5 years, Celsius Holdings has seen intense revenue growth. The company also turned a refreshing operating and net profit in 2023 after years of unprofitability:

Notable 5-Year Growth Figures:

- Revenue: 90.4% CAGR (compound annual growth rate) Absurd revenue growth.

- Operating Income: N/A (negative operating profits)

- Net Income: N/A (negative net profits)

See Celsius Holdings’s full financial history >>>

Celsius’s revenues have nearly doubled every year over the last 5 years.

And the company is now turning an operating and net profit.

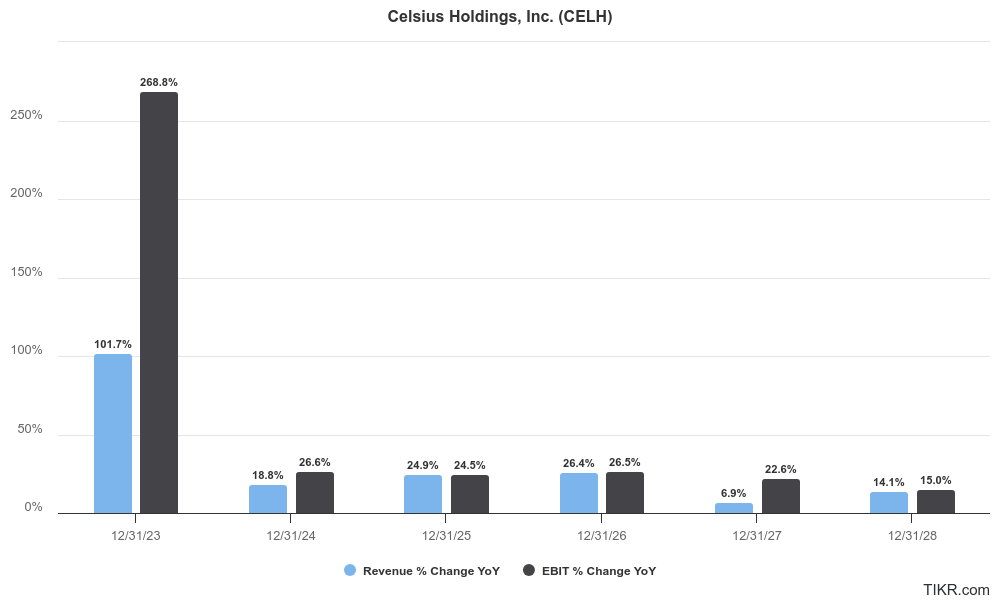

Analysts expect the company to see just about 20% annual revenue and operating income growth over the next few years, which is still above-average growth:

Notable 3-Year Forecast Figures:

- Revenue: 18.0% CAGR

- Operating Income: 23.0% CAGR

Notable 5-Year Forecast Figures:

- Revenue: 23.3% CAGR

- Operating Income: 25.9% CAGR

See Celsius’s full analyst estimates >>>

Is Celsius a high-quality business?

Is it too early to tell if Celsius will be a high-quality business because the company only has one year of real profitability?

We can still look at analyst estimates to see if the company is expected to generate strong profits in the future.

We also have another trick for determining whether the company has a high-quality business model, but we’ll look at that later.

First, return on equity (ROE) is one of our favorite profitability measures because it measures how efficiently a company creates profit from its shareholders’ equity.

The formula for ROE is simply Net Income / Average Shareholders’ Equity.

Celsius Holdings only saw a sizeable net income just last year. Shareholders will ultimately have to wait and see if the company sustains a high level of profitability.

However, analysts expect Celsius to see a strong return on equity over the next several years, with a 38.8% ROE in the next full fiscal year. This is above average:

We like to look for companies that can sustain over 20% returns on capital. Analysts expect Celsius Holdings to see a fiery 30%+ return on equity in the next few fiscal years, which means the company should also see strong returns on capital.

Gross Margins (High-quality business detector)

Gross margins are one of the easiest ways to see if a company has a high-quality business.

It measures the percentage of revenue left over as profit after a company pays the material and service costs directly tied to creating and delivering products or services, also known as its cost of goods sold (COGS).

A company with low gross margins generally operates in a commoditized industry, while a business with high gross margins comfortably sells products for much more than they cost to produce.

That’s why it works as a high-quality business detector.

In the past 5 years, Celsius Holdings has seen gross margins in the low to mid-40s. Now, in the next 5 years, analysts expect gross margins to rise to the high 40s and even hover around 50%:

Check out Celsius’s full profitability analysis >>>

We’ve found that decent businesses have 30% or higher gross margins, while excellent businesses tend to have 50% or higher margins.

That means it’s a great sign that Celsius has been seeing over 40% gross margins, and analysts expect gross margins to rise to a fearless 50% for fiscal year 2026.

Is Celsius a buy right now?

Today, analysts give $CELH a consensus price target of about $62. With Celsius Holdings trading around $38 per share, this implies that there’s a 62.4% upside for shares to reach fair value.

These consensus estimates are aggregated by Wall Street’s sell-side analyst estimates, meaning they’re stock price estimates made by real people. Analysts often get stock forecasts wrong, but it’s still a fairly reliable place to start to see if a stock might be undervalued.

Based on analysts’ price targets, Celsius Holdings has had an average upside of 38.5% over the past five years. This is a bullish sign because analysts estimate the stock has a bigger upside than usual.

You can see in the graph below that analysts see a higher upside for $CELH right now than they have in the past year:

Analysts see more upside in Celsius Holdings stock today than in the past year, with the stock’s current share price of $38/share.

See $CELH’s full analyst price targets >>>

Right now, you might wonder if there‘s a better way to value the stock than by examining analysts’ estimates alone.

There are two more quick ways we like to check to see if a stock might be undervalued.

EV/Revenue Multiple:

How do you know if a company’s expected revenue growth is already factored into the price?

For this, we like to look at a company’s NTM EV/Revenue, which looks at a company’s current enterprise value, which is the total capital invested in the business (Market Cap + Total Debt – Cash), and divided by analysts’ consensus estimates for the company’s next twelve months’ revenue.

Basically, NTM EV/Revenue takes the business’s total value and divides it by expected revenue for the next 12 months. $CELH is trading 49.7% below its 5-year average of 10.1x. This suggests Celsius could be undervalued:

Check out $CELH’s full valuation analysis >>>

P/E Multiple:

Still, it’s good to fact-check valuation methods to ensure a stock is undervalued.

We have limited options for valuing the company because the company only turned a substantial operating and net profit last year.

Still, we’ll look at the company’s NTM P/E ratio for the past year. This divides the company’s current share price by analysts’ consensus estimates for its next twelve months’ earnings per share.

CELH is trading 47.1% below its 1-year average NTM P/E. This suggests CELH could be slightly undervalued:

Celsius Holdings is trading at its lowest NTM P/E ratio in the past year. This doesn’t necessarily mean the stock is undervalued, but it is certainly a good sign.

Check out Celsius Holdings’s full valuation analysis >>>

Takeaway

Today, analysts estimate that Celsius Holdings has about 62% upside, and the stock is currently trading nearly 50% below its 5-year average NTM EV / Revenue multiple.

Celsius’s revenues have nearly doubled every year for the past 5 years, and now analysts expect revenues to grow around 20% annually while attaining higher gross margins.

The TIKR Terminal offers industry-leading financial data on $CELH and over 100,000 other stocks.

So if you’re looking to analyze and find the best stocks for your portfolio, you’ll want to use TIKR!

TIKR offers institutional-quality research with a simple platform made for individual investors like you.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. We aim to provide informative and engaging analysis to help empower individuals to make their own investment decisions. Neither TIKR nor our authors hold any positions in the stocks mentioned in this article. Thank you for reading, and happy investing!