Lululemon (LULU) beat earnings and revenue expectations in Q4, with impressive margin improvements. However the stock is down 10% in pre-market after the company issued weak guidance for 2025’s calendar year.

While the athletic apparel maker delivered solid results, management explained that economic uncertainty and inflation concerns might impact consumer spending.

So, is now the time to buy Lululemon stock?

See Lululemon’s full financials, growth trends, and analyst forecasts on TIKR >>>

Q4 Notable Points:

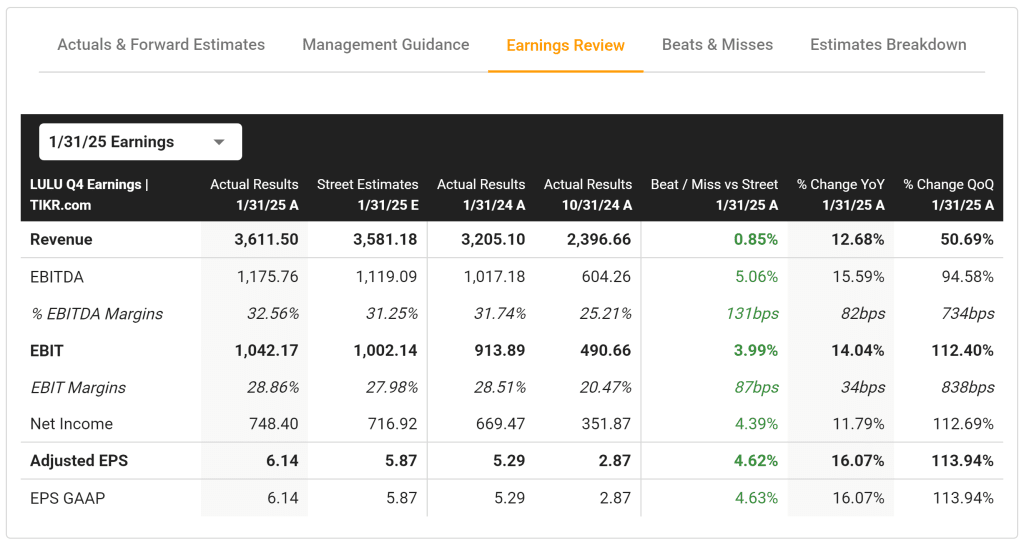

- Revenue: $3.61B (0.85% estimate beat) (up 12.68% from last year)

- Operating Margins: 28.86% (399 basis points estimate beat) (up 131 basis points from last year)

- Adjusted EPS: $6.14 (4.62% estimate beat) (up 16.07% from last year’s same quarter)

View the full Q4 earnings results >>>

Lululemon Faces Growth Challenges

Lululemon delivered impressive fourth-quarter results, but a disappointing guidance raises concerns about future growth. CEO Calvin McDonald acknowledged the challenges during the earnings call, stating:

“There continues to be considerable uncertainty driven by macro and geopolitical circumstances. That being said, we remain focused on what we can control.”

See the full earnings transcript >>>

1. US Market Saturation Is Limiting Growth

Lululemon’s comparable sales in the Americas were flat in Q4, indicating the athleisure giant is hitting growth limitations in its core market.

The brand’s premium positioning makes Lululemon vulnerable to economic pressures, as McDonald noted that consumers are spending less due to inflation concerns.

Lululemon must accelerate its international expansion efforts to maintain momentum while finding new ways to stimulate domestic demand.

Get advanced business insights with TIKR >>>

2. International Expansion Is the Bright Spot

Lululemon’s international business grew 20% in comparable sales during Q4, demonstrating the brand’s global appeal.

This year, it plans to expand to Italy, Denmark, Belgium, Turkey, and the Czech Republic, which should help offset the domestic slowdown. This international runway remains Lululemon’s most promising growth opportunity as the US market matures.

3. Margin Pressure Will Impact 2025 Results

CFO Meghan Frank warned that gross margins are expected to fall 0.6 percentage points in 2025 due to higher fixed costs, foreign exchange rates, and US tariffs on China and Mexico.

This margin contraction and slower growth explain why Lululemon’s guidance disappointed Wall Street.

To protect its profitability, Lululemon must balance growth investments with operational efficiency.

Analyze stocks quicker with TIKR >>>

TIKR Takeaway

Lululemon delivered strong Q4 results with impressive profitability but faces headwinds from economic uncertainty and US market saturation.

Is Lululemon a buy despite its disappointing guidance? Use TIKR to analyze the company’s international growth potential, margin trends, and valuation metrics.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!