Key Takeaways:

- The 2-Minute Valuation Model values Intel stock at $28/share in 2 years.

- This implies that the stock could have nearly 40% upside from its current share price.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Intel’s stock has dropped nearly 60% just this year, driven by stagnant revenue growth and shrinking earnings. The company is dealing with operational challenges, including supply chain issues and a slower-than-expected turnaround in its manufacturing technology.

Intel is also expected to face tougher competition in the semiconductor market, particularly from rivals like AMD and TSMC, which continue to gain market share.

Intel’s stock might look undervalued today, but it comes with a cautionary tale. Over the past 10 years, Intel stock has delivered a negative return, even after accounting for dividends.

Morningstar has removed its economic moat rating for Intel, citing that “We don’t believe the company will generate excess returns on capital in the next three to five years (even when considering government subsidies and other incentives).”

The problem with companies that lack a strong economic moat is that even when they invest heavily to grow, they often struggle to generate strong profits. This can lead to significant spending with little payoff, resulting in mediocre returns at best.

That’s why it might be wise to wait and see if Intel can reclaim its position as a market leader in core markets before investing. While the company’s risk of bankruptcy is low, the bigger concern is that Intel’s stock could continue to stagnate or decline, leaving investors with poor returns.

That means investors would have missed out on the opportunity to invest in strong companies that do have competitive advantages and will likely see higher returns.

We like AMD & Nvidia better than Intel. Find the best stocks to buy today! >>>

What is the 2-Minute Valuation Model?

There are 3 core factors that drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

The 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized EPS, and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Intel Could be Undervalued

Forecast

On Intel’s Analyst Estimates tab shown below, you can see that analysts expect the company to grow revenue at a 5.8% compound annual growth rate, and EPS is expected to rebound back to profitability:

View Intel’s full analyst estimates >>>

For context, revenue declined at an average annual rate of 6.1% over the past 5 years, so revenue growth would really help to stabilize the company.

Valuation Multiple

Today, Intel trades at around $20 per share, which means the stock trades at just over 2 times next year’s expected revenue and nearly 29 times next year’s expected earnings.

The stock has averaged a 177x forward P/E multiple over the past 10 years:

Value stocks quicker with TIKR >>>

We’ll use a 15x forward P/E ratio in our valuation to represent the stock’s normalized, long-term P/E ratio.

Fair Value

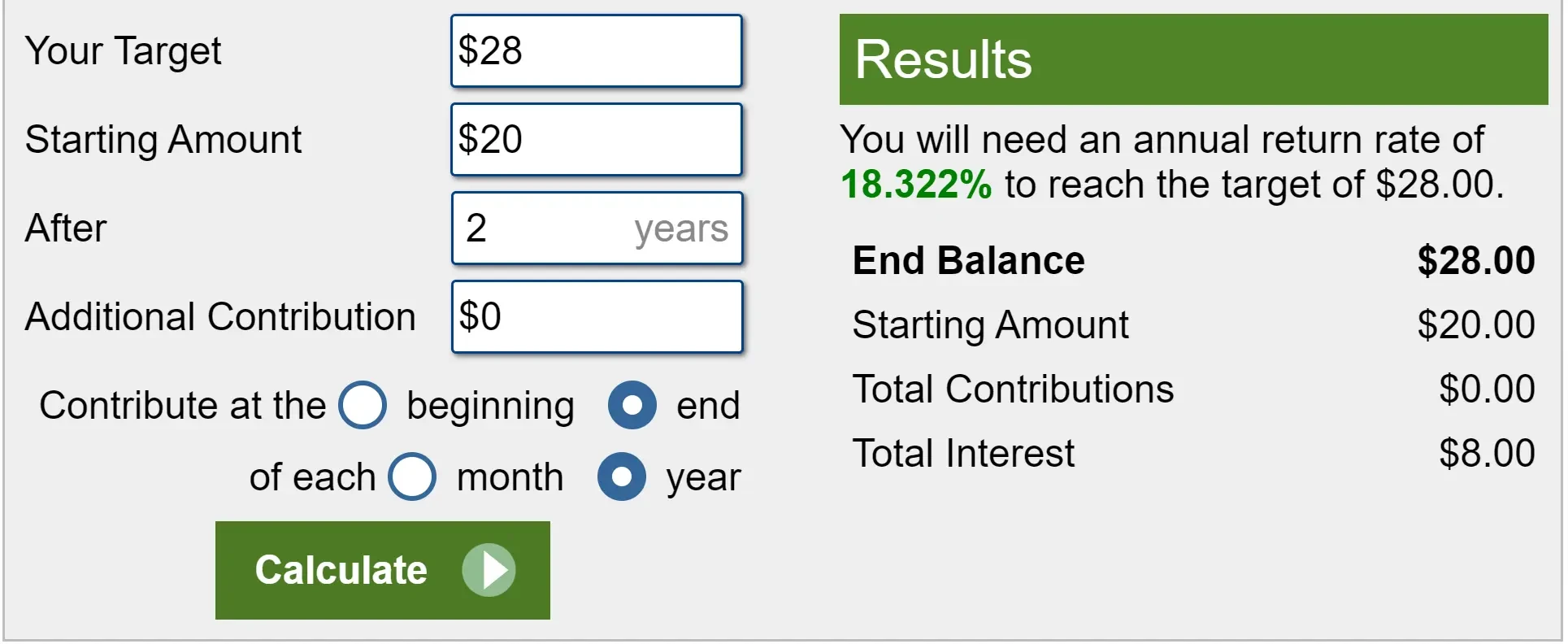

3 years from now, analysts estimate that Intel is expected to reach about $1.88 in normalized EPS. At a 15x NTM P/E multiple, that values Intel stock in 2 years at $28/share.

(The NTM P/E multiple uses the expected earnings for the next twelve months, so a 2-year valuation uses 3-year EPS forecast figures.)

With the stock trading at about $20 today, this implies that Intel could rise 18.3% per year over the next 2 years, or 40% in total, to reach this fair value:

The market has averaged about 10% annual returns over the long run, so 18% annual returns would be really impressive.

Analysts have a price target of $24/share for Intel stock, but analysts have had a historically difficult time valuing the stock.

Find the best stocks to buy today with TIKR >>>

Analysts’ Price Target

The consensus analyst price target for Intel today is about $24 per share, which means analysts think the stock has about 20% upside

The blue line in the graph below shows analysts’ estimated upside for Intel stock.

When the blue line was high, analysts thought Intel stock was undervalued. When the blue line was low, they thought Intel stock was overvalued.

The black line simply tracks Intel’s stock price.

You can see that analysts correctly thought that Intel was undervalued towards the end of 2022. With Intel’s recent price drop, analysts think the stock is undervalued again:

Analysts’ price targets can suffer from many biases and aren’t always accurate.

Still, looking at analysts’ consensus price targets can be a great way to get a “second opinion” on your own stock valuation.

TIKR Takeaway

Based on the 2-Minute Valuation Model, it looks like Intel stock could be undervalued today, and it’s possible that the stock could go up 40% in the next 2 years.

This is, of course, just a valuation exercise. No one knows where a stock is headed in the short term, and few can predict where a stock is heading in the long term.

Investors should also keep in mind that Intel no longer has a moat, which means it could lose to competitors over the long term.

We like AMD & Nvidia better than Intel. Find the best stocks to buy today! >>>

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. We aim to provide informative and engaging analysis to help empower individuals to make their own investment decisions. Neither TIKR nor our authors hold positions in any of the stocks mentioned in this article. Thank you for reading, and happy investing!