Key Takeaways:

- The 2-Minute Valuation Model values Starbucks at $144/share in 2.75 years.

- This implies that the stock could have nearly 60% upside from its current share price.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Starbucks’ stock is down nearly 20% over the past three years, because even though revenue has grown 20% over this period, earnings have stayed flat. Starbucks faces operational challenges, like labor disputes and strategic hurdles, and Starbucks is expected to face growing competition in China from both local and international rivals, which could add pressure moving forward.

Nevertheless, Morningstar continues to rate Starbucks as a wide-moat company due to its strong loyalty program and scale-driven cost advantages.

Starbucks remains a leader in the coffee industry. Today, it looks like Starbucks is slightly overvalued.

What is the 2-Minute Valuation Model?

There are 3 core factors that drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

The 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized EPS, and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Starbucks Looks Undervalued

Forecast

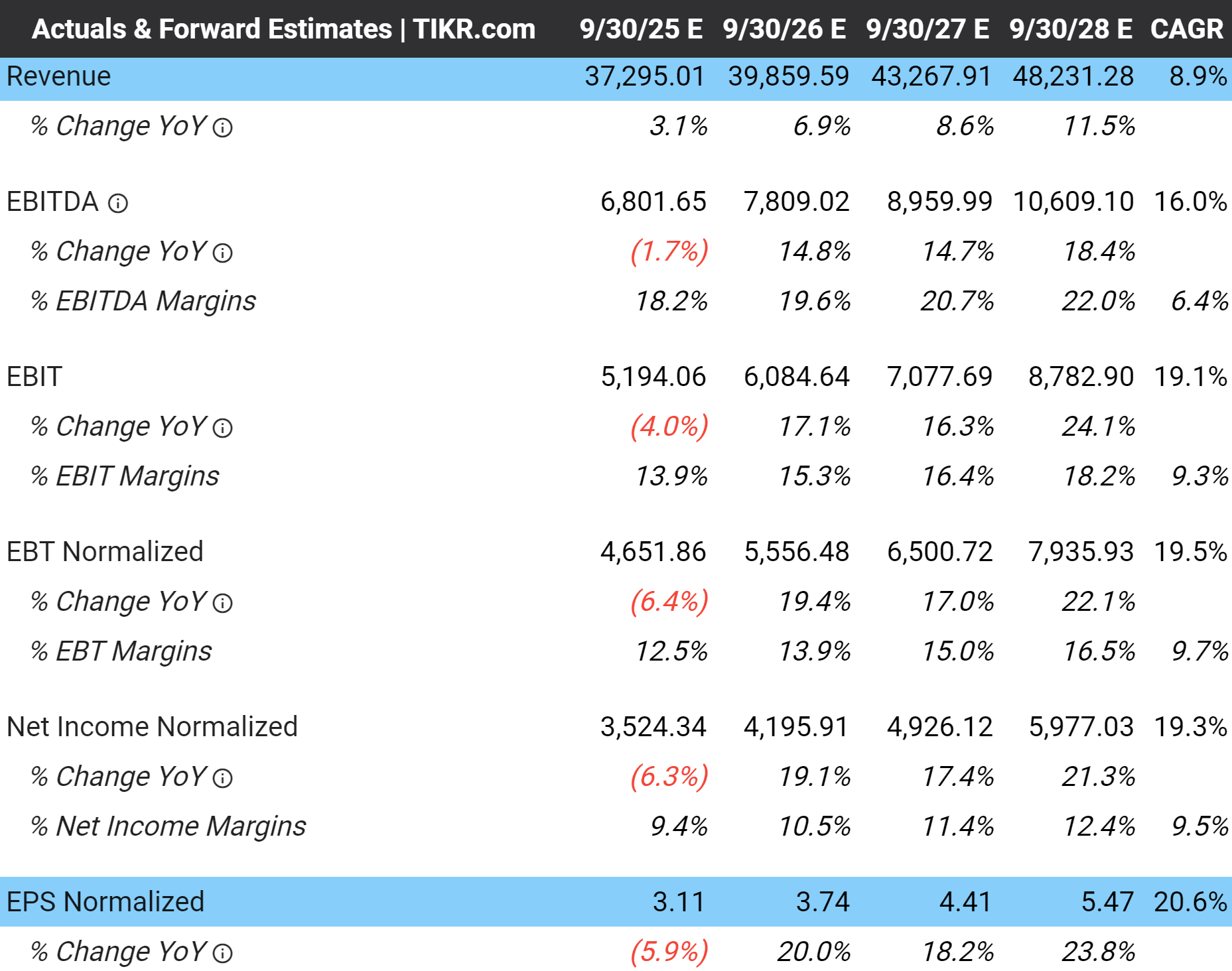

On Starbucks’ Analyst Estimates tab shown below, you can see that analysts expect the company to grow revenue at an 8.9% compound annual growth rate over the next 3 years. Normalized earnings per share, or EPS, is expected to grow considerably faster at 20.6% annually as profit margins are expected to rebound back to previous levels:

View Starbucks’ full analyst estimates >>>

For context, revenue grew at 6.4% annually over the past 5 years, so the company’s expected growth is pretty similar to historical growth.

Valuation Multiple

Today, Starbucks trades at around $91 per share, which means the stock trades at just over 3 times next year’s expected revenue and slightly above 29 times next year’s expected earnings.

The stock has averaged a 25.7x forward P/E multiple over the past 3 years:

Value stocks quicker with TIKR >>>

We’ll use a 25x forward P/E ratio in our valuation, since the stock is expected to see about the same growth going forward as it has in the past 5 years.

Fair Value

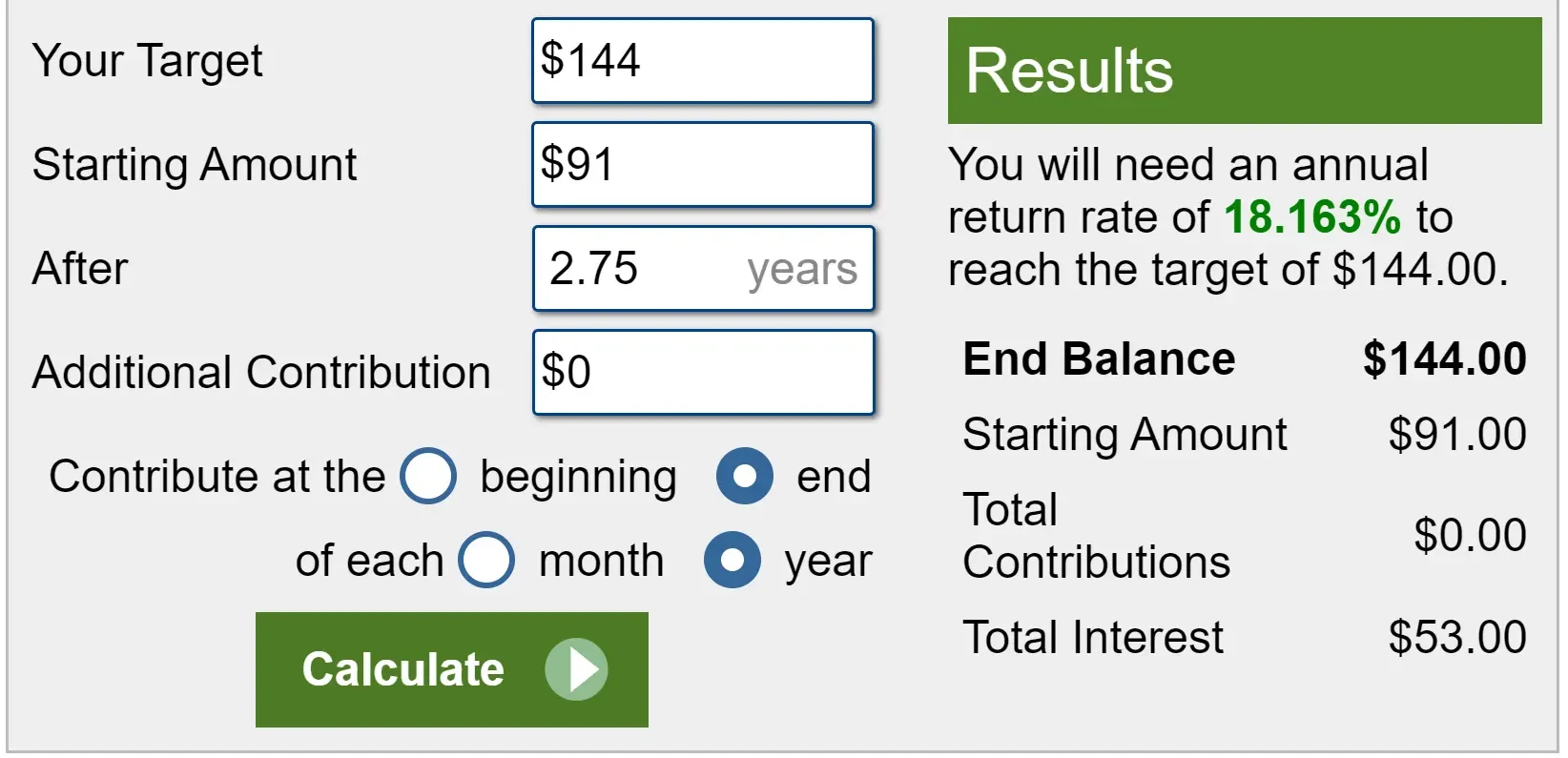

3.75 years from now, analysts estimate that Starbucks is expected to reach about $5.47 in normalized EPS. At a 25x NTM P/E multiple, that values Starbucks stock in 2.75 years at $137/share. When we tack on Starbucks’ expected dividends over this time of about $7/share, we’re left with a final fair value of $144/share for Starbucks.

(The NTM P/E multiple uses the expected earnings for the next twelve months, so a 2.75-year valuation uses 3.75-year EPS forecast figures. We’re using a 2.75-year valuation because Starbucks’ fiscal year ends in September, three-quarters of the way through the year.)

With the stock trading at about $91 today, this implies that Starbucks could rise 18.2% per year over the next 2.75 years, or 58% in total, to reach this fair value:

The market has averaged about 10% annual returns over the long run, so 18% annual returns would be really impressive.

Analysts are less optimistic on Starbucks’ stock, but they also think the stock is undervalued.

Find the best stocks to buy today with TIKR >>>

Analysts’ Price Target

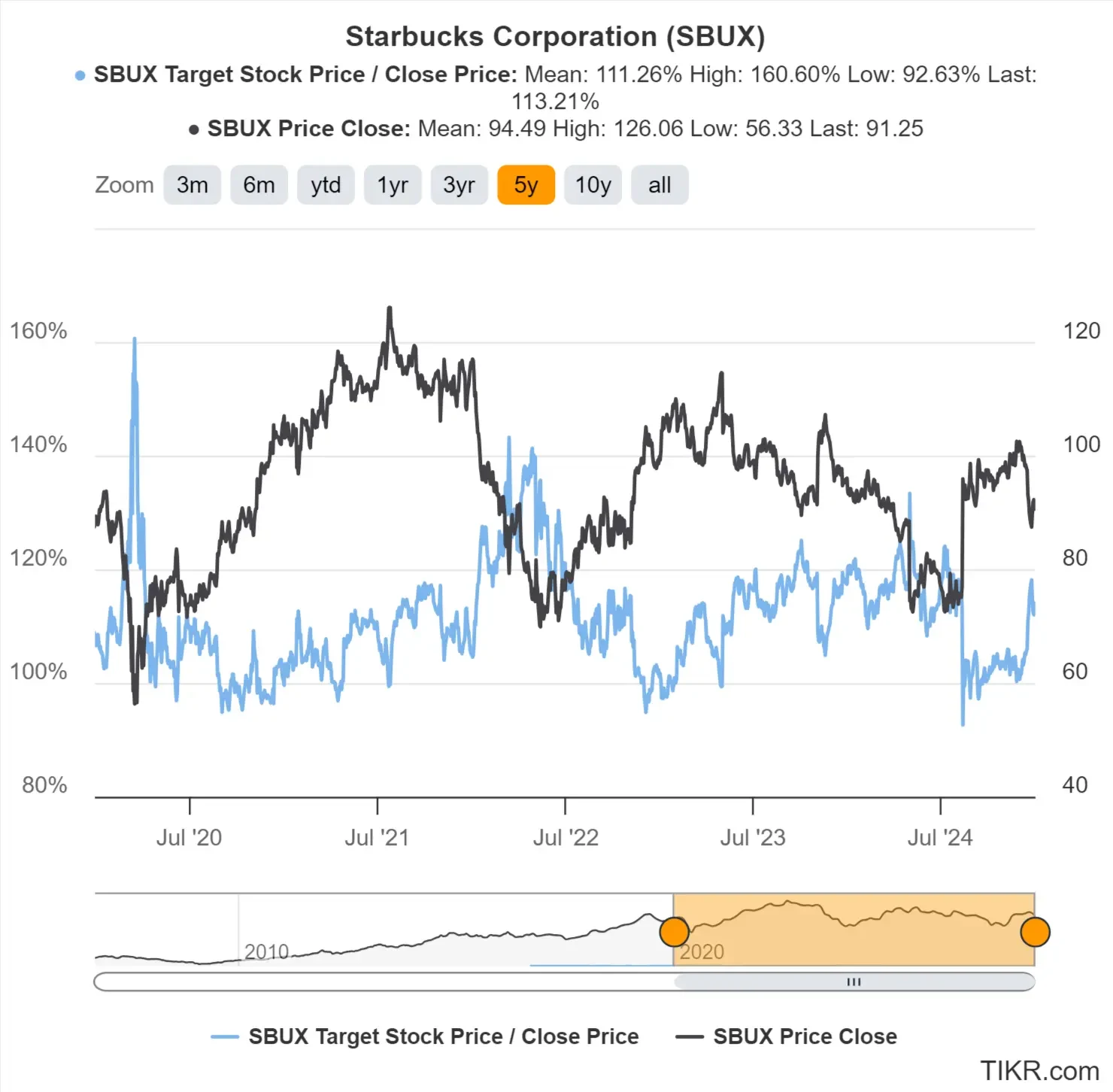

The consensus analyst price target for Starbucks today is about $103 per share, which means analysts think the stock has about a 13% upside from Starbucks’ current share price of $91.

The blue line in the graph below shows analysts’ estimated upside for Starbucks stock. When the blue line was high, analysts thought the stock was undervalued, while when the blue line was low, they thought Starbucks stock was overvalued. The black line is simply Starbucks’ stock price.

You can see that analysts correctly thought that Starbucks was undervalued in mid-2022 and mid-2024. With Starbucks’ recent price drop, they think the stock is undervalued again:

Analysts’ price targets can suffer from many biases and aren’t always accurate.

Still, looking at analysts’ consensus price targets can be a great way to get a “second opinion” on your own stock valuation.

TIKR Takeaway

Based on the 2-Minute Valuation Model, it looks like Starbucks stock is undervalued today, and the stock could go up nearly 60% in a little less than 3 years.

This is, of course, just a valuation exercise. No one knows where a stock is headed in the short term, and few can predict where a stock is heading in the long term.

Don’t take our word for it—try it out for yourself! Analyze Starbucks or any stock you’re interested in on TIKR today!

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. We aim to provide informative and engaging analysis to help empower individuals to make their own investment decisions. Neither TIKR nor our authors hold positions in any of the stocks mentioned in this article. Thank you for reading, and happy investing!