Key Takeaways:

- The 2-Minute Valuation Model values Amazon stock at $272/share in 2 years, implying 25% upside today.

- Amazon has averaged 28% annual returns over the past decade, so it’s not hard to imagine that the stock could see 12% annual returns over the next 2 years.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

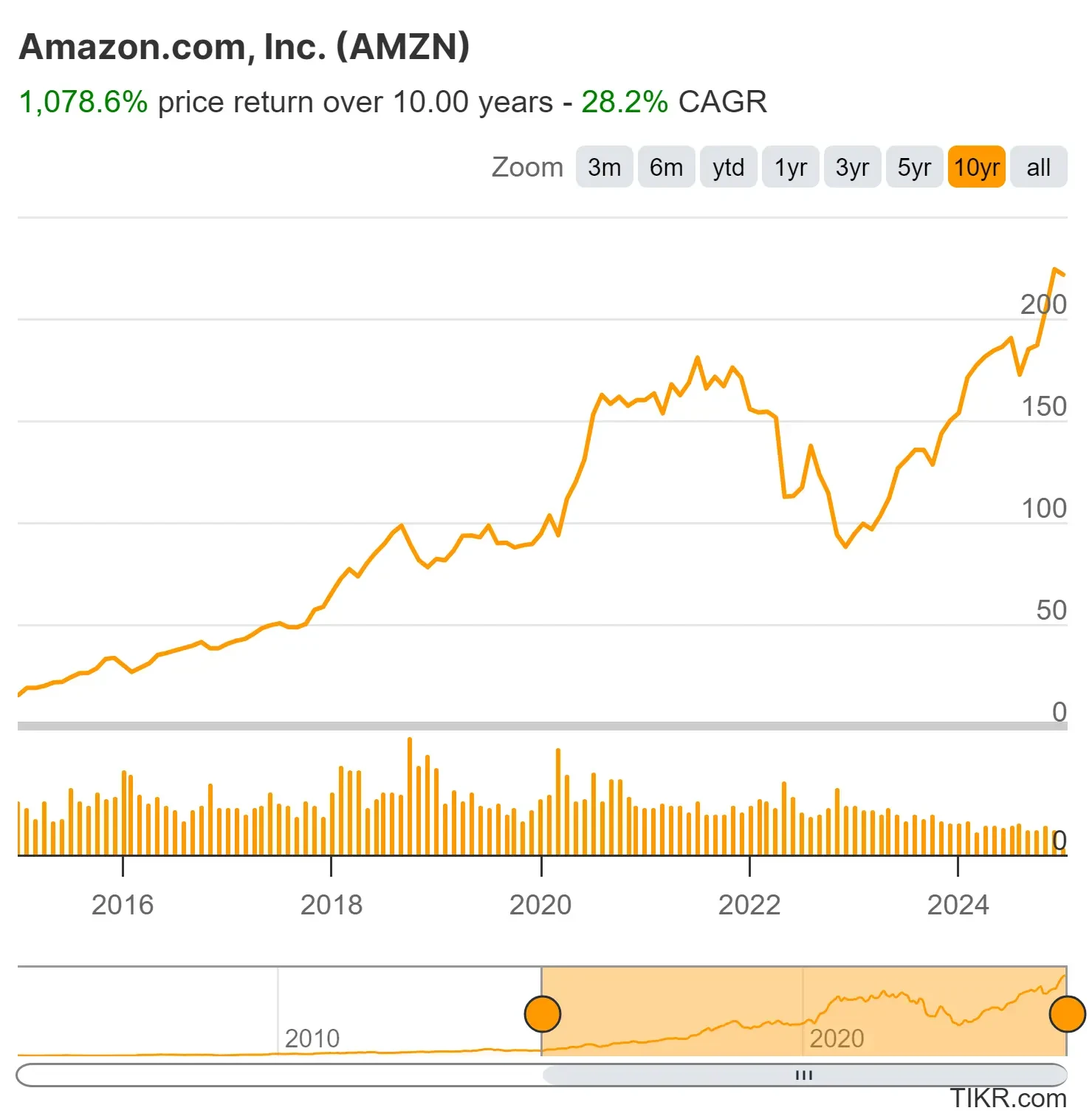

Amazon (AMZN) has delivered an impressive 28% average annual return over the past decade, driven by its e-commerce dominance and the rapid growth of Amazon Web Services (AWS).

Amazon looks slightly undervalued today, with analysts expecting 20% annual earnings growth ahead.

That said, the company faces challenges in keeping up its cloud growth as competition from Microsoft Azure and Google Cloud increases, along with macroeconomic pressures that could affect consumer spending.

Even with these hurdles, Amazon remains a global leader in innovation, with big opportunities in cloud computing, logistics, and AI.

At its current valuation, the stock could be a great long-term opportunity for investors looking for quality and growth.

Amazon stock could be undervalued. See how you can value stocks quicker with TIKR! >>>

What is the 2-Minute Valuation Model?

There are 3 core factors that drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized EPS, and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Is Amazon Undervalued?

Forecast

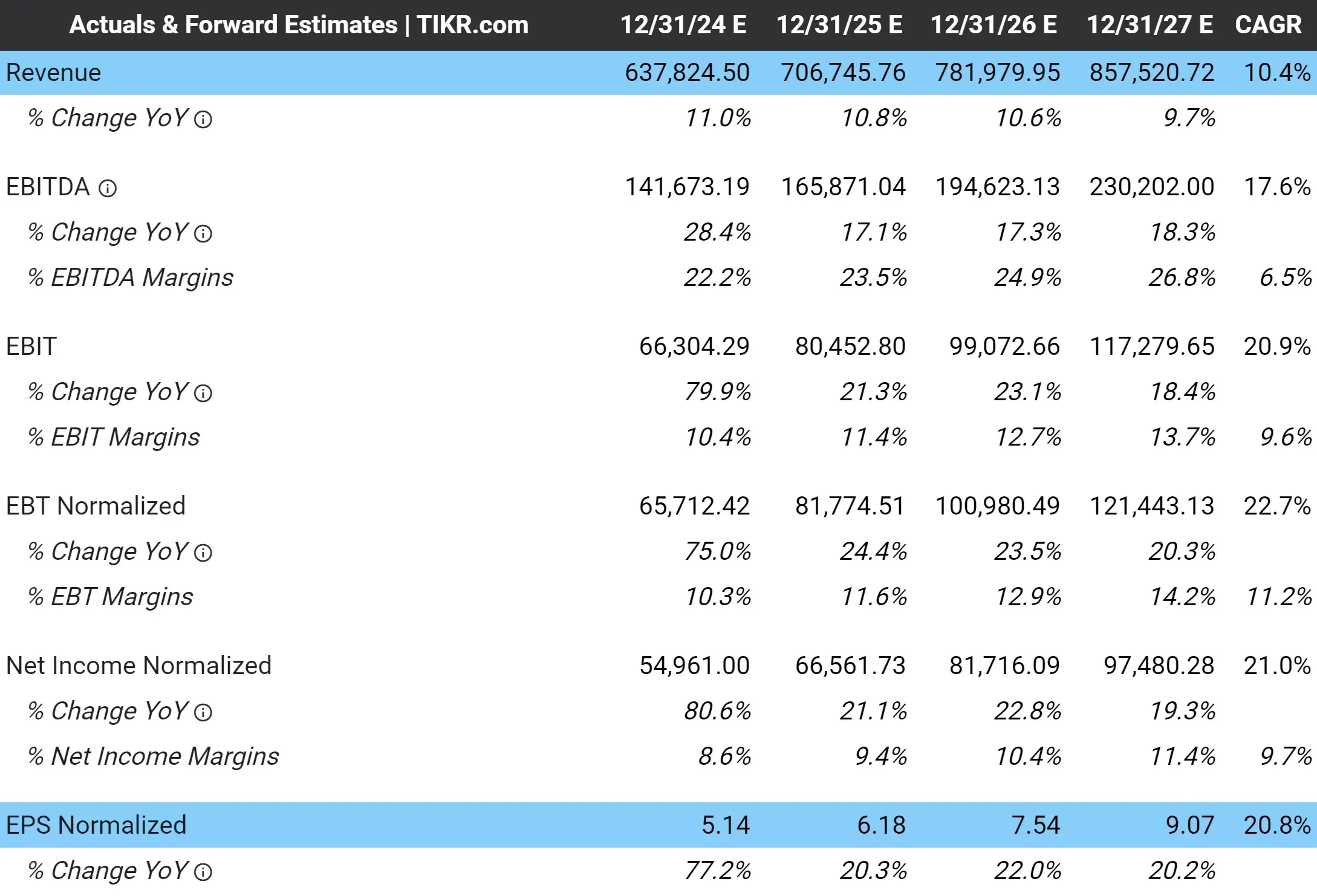

On Amazon’s Analyst Estimates tab shown below, you can see analysts expect the company to grow revenue at a 10% compound annual growth rate over the next 3 years, while normalized earnings per share, or EPS, are expected to grow at nearly 21% annually due to Amazon’s increasing profit margins:

View Amazon’s full analyst estimates >>>

For context, over the past 5 years, Amazon’s revenue grew at 18% per year, while normalized earnings grew at 35% per year. That means Amazon’s growth is expected to slow down slightly.

Still, 10% annual revenue growth and 20% annual EPS growth are impressive metrics, especially for a $2.3 trillion company.

Valuation Multiple

Amazon currently trades at around $218 per share, which means the stock trades at about 3.5 times next year’s expected revenue and 37 times next year’s expected earnings.

With 20% expected EPS growth, a 37x earnings multiple seems fairly reasonable.

In today’s market, high-quality blue-chip stocks often trade at a P/E ratio of roughly 2x their annual EPS growth.

While that might seem expensive, Amazon stands out as one of the most proven companies in the United States, which remains the world’s most desirable equity market.

Put simply, investors are paying up to own high-quality American companies.

Amazon has averaged a 66x forward P/E multiple over the past 5 years, but let’s take a more conservative approach and use a 30x P/E multiple in our valuation. This represents 1.5x Amazon’s expected EPS growth, which is cheaper than the multiples we’re seeing for most Big Tech companies:

Fair Value

3 years from now, analysts estimate that Amazon could reach about $9.07 in normalized EPS. At a 30x NTM P/E multiple, that values Amazon stock in 2 years at $272/share.

(The NTM P/E multiple uses the expected earnings for the next twelve months, so a 2-year valuation uses 3-year EPS forecast figures.)

With the stock trading at about $218 today, this implies that $AMZN could rise about 11.7% per year over the next 2 years, or 25% in total:

Amazon is expected to grow earnings at 20% annually. Even if the stock starts trading at a lower valuation multiple, it makes sense that 20% earnings growth will drive double-digit returns.

Analysts aren’t quite as bullish on Amazon, but they still think the stock has upside today.

Analysts’ Price Target

The consensus analyst price target for Amazon today is about $245 per share, which means analysts think the stock has just over 10% upside.

The blue line below shows analysts’ estimated upside for $AMZN stock over the past 5 years.

When the blue line was high, analysts thought Amazon stock was undervalued. When the blue line was low, analysts thought Amazon was overvalued.

The black line simply tracks Amazon’s stock price, which you can see crashed in 2022 and rebounded nearly 200% from its low point.

Analysts thought Amazon was undervalued towards the end of 2022, and they think the stock has around 12% upside today:

Find the best stocks to buy today with TIKR >>>

TIKR Takeaway

Using the 2-Minute Valuation Model, Amazon stock appears slightly undervalued and could deliver 12% annual returns over the next 2 years.

Of course, this is just a valuation exercise. No one knows where a stock is headed in the short term, and few can predict where a stock is heading in the long term.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. We aim to provide informative and engaging analysis to help empower individuals to make their own investment decisions. Neither TIKR nor our authors hold positions in any of the stocks mentioned in this article. Thank you for reading, and happy investing!