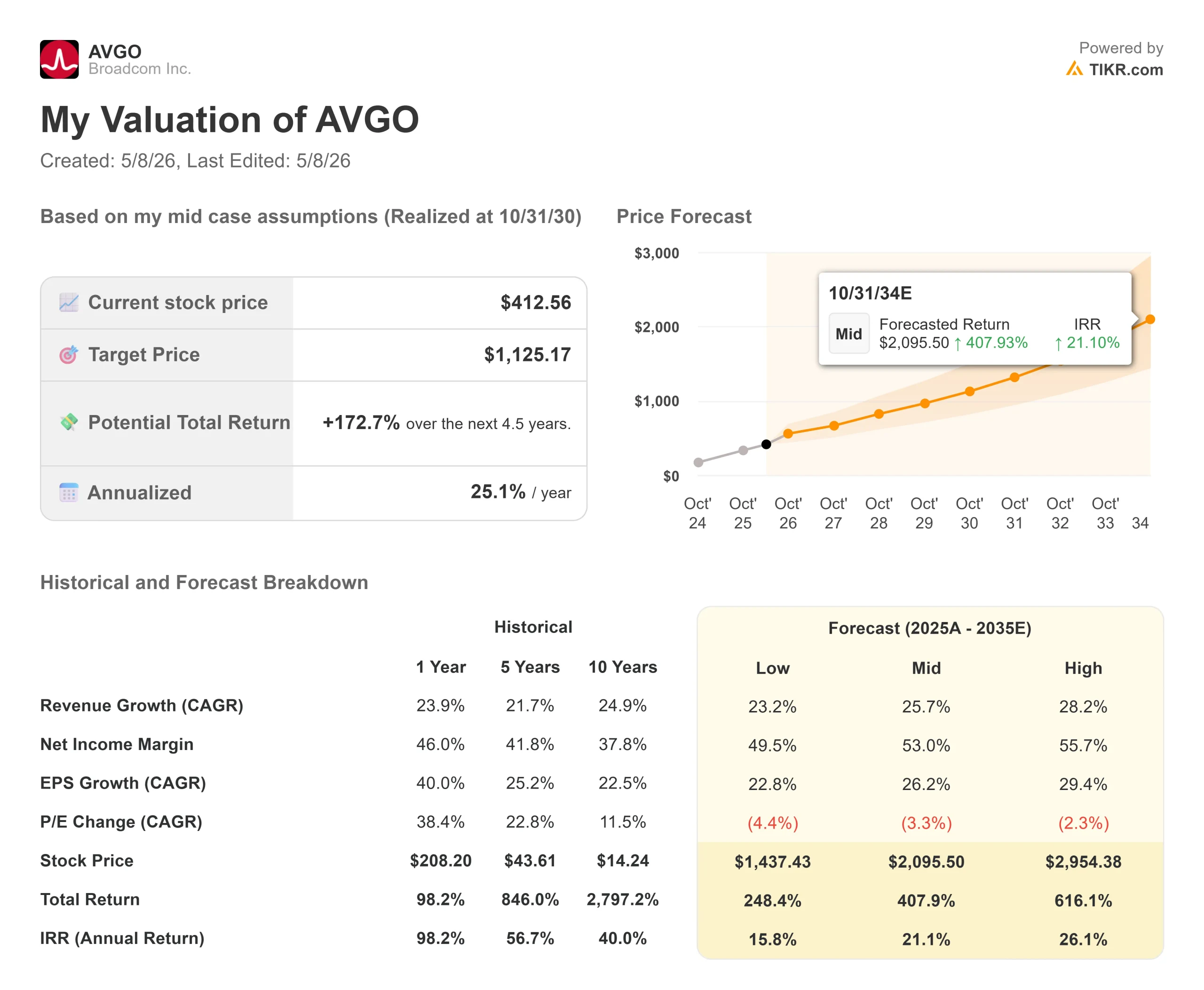

Key Stats for Broadcom Stock

- Current Price: $412.56

- Target Price (Mid): ~$1,125

- Street Target: ~$475

- Potential Total Return: ~173%

- Annualized IRR: ~25% / year

- Earnings Reaction: +4.80% (March 4, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Broadcom (AVGO) fell around 3% to 4% on Thursday, May 7, after The Information reported that its custom AI chip deal with OpenAI, codenamed Project Nexus, has hit an $18 billion financing roadblock. The stock closed at $412.56. Bulls called it an overreaction to one customer’s financing complexity. Bears said it confirmed the customer concentration risk they had been flagging for months. The central question: if OpenAI stumbles, does Broadcom’s $100 billion AI chip story for 2027 still hold?

According to The Information, Broadcom will only finance the first phase of chip production if Microsoft agrees to buy roughly 40% of the output. That first phase covers 1.3 gigawatts of data center capacity and costs approximately $18 billion. Microsoft has not signed a firm purchase agreement, and the two sides are stuck on a fundamental infrastructure disagreement: OpenAI wants data centers optimized for its custom silicon, while Microsoft prefers standard, versatile designs. Broadcom’s investor relations materials confirm the next opportunity for management to address this publicly is the June 3, 2026, Q2 earnings call.

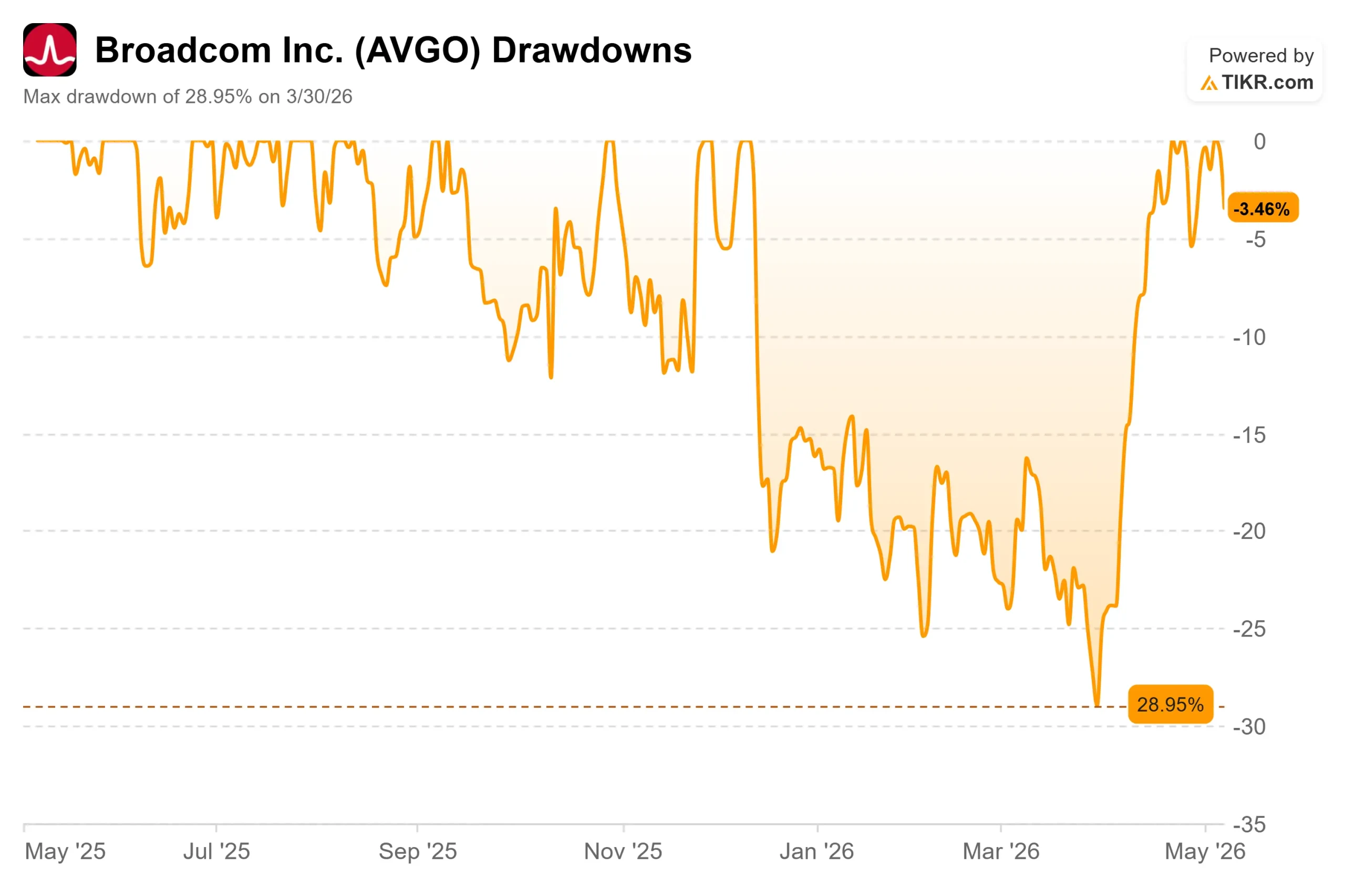

The sell-off landed on a stock that had already recovered significantly. Broadcom hit a max drawdown of 28.95% on March 30, 2026, and had climbed back toward its 52-week high of $437.68 before Thursday’s drop. The question now is whether the OpenAI snag is a structural problem or a deal mechanic that gets resolved.

See historical and forward estimates for Broadcom stock (It’s free!) >>>

What Hock Tan Actually Said About OpenAI

To understand whether the sell-off was rational, you need to look at what CEO Hock Tan said on the Q1 fiscal 2026 earnings call on March 4, 2026.

Tan announced OpenAI as Broadcom’s sixth major AI customer, describing the engagement as strategic and multiyear. “We expect OpenAI deploying in volume their first-generation XPU in 2027 at over 1 gigawatt of compute capacity,” he said. That is a 2027 deployment event. The Project Nexus financing snag, if unresolved, affects future delivery timelines, not the AI revenue Broadcom is already guiding for in Q2 FY2026.

Tan was explicit that OpenAI is the sixth and newest customer, not the largest or most critical. For Google, he described “strong demand for the seventh-generation Ironwood TPU,” with even stronger generations expected in 2027 and beyond. For Anthropic, he said Broadcom is “off to a very good start in 2026 for one gigawatt of TPU compute,” with demand expected to “surge in excess of 3 gigawatts” in 2027. For Meta, Tan pushed back on analyst skepticism directly: “contrary to recent analyst reports, Meta’s custom accelerator MTIA road map is alive and well.” For customers four and five, shipments are strong and “expected to more than double in 2027.”

That Q2 guide calls for $10.7 billion in AI semiconductor revenue, up around 140% year over year. None of those figures depends on OpenAI, which was not yet a volume customer at the time of the March call. On the total 2027 picture, Tan said Broadcom has “line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027.” He added that the company’s 2027 gigawatt visibility across all six customers is approaching 10 gigawatts. Even if OpenAI’s 1 gigawatt slips, the remaining five provide the other nine.

The Networking Business the Snag Does Not Touch

AI networking is a separate Broadcom revenue stream that Thursday’s news did not affect at all. In Q1, AI networking revenue grew 60% year over year and represented one-third of total AI revenue. In Q2, management projected that the share would rise to 40%.

The driver is Broadcom’s Tomahawk 6 switch, which operates at 100 terabits per second. Broadcom also leads in 200G SerDes technology (serializer/deserializer, the high-speed signal processing that connects chips within and between server racks), with a 400G version already operational and a next-generation Tomahawk 7, offering double the performance, planned for 2027. This networking advantage applies to customers running both custom XPUs and Nvidia GPUs, so Broadcom captures AI infrastructure spending regardless of which chip architecture wins.

Tan was asked directly whether customer-owned tooling programs, where hyperscalers attempt to build their own silicon, could displace Broadcom. His answer: “We will not see competition in COT for many years to come.” His reasoning was not just about design capability but production scale. “Anybody can design a chip in a lab that works well. Can you produce 100,000 of those chips quickly at yields that you can afford? We don’t see too many players in the world that can do that.”

Sitting behind the semiconductor business is a software layer with its own defensibility. VMware Cloud Foundation (VCF), the private cloud software Broadcom acquired with VMware, generated $6.8 billion in Infrastructure Software revenue in Q1, up 1% year over year, with annual recurring revenue growing 19% year over year. Software gross margins reached 93% in Q1. Tan argued VCF becomes more essential as AI workloads enter enterprise data centers, not less: “VCF cannot be disintermediated or replaced.”

How Broadcom Is Priced Against Peers

TIKR’s Competitors page shows Broadcom trading at 24.33xNTM EV/EBITDA (enterprise value divided by the next twelve months of earnings before interest, taxes, depreciation, and amortization). NVIDIA sits at 20.25x and AMD at 40.10x on the same metric. On NTM P/E, Broadcom is at 30.63x versus Nvidia’s 25.36x and AMD’s 47.00x.

Broadcom’s roughly 4-turn premium to Nvidia on NTM EV/EBITDA is modest given that TIKR shows Broadcom’s forward two-year revenue CAGR at 57.5%. On both EV/EBITDA and P/E, Broadcom trades at a meaningful discount to AMD, though AMD’s growth profile and margin structure differ enough that direct comparison has limits. Whether Broadcom’s premium to Nvidia is justified comes down to how much weight investors place on the OpenAI financing uncertainty versus the five other customer ramps already in motion.

See how Broadcom performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $412.56

- Target Price (Mid): ~$1,125

- Potential Total Return: ~173%

- Annualized IRR: ~25% / year

See analysts’ growth forecasts and price targets for Broadcom stock (It’s free!) >>>

The TIKR mid-case model uses the 10/31/30 horizon and targets approximately $1,125 per share. The two primary revenue CAGR drivers are AI semiconductor revenue, projected at roughly 26% annual growth through 2030 across six XPU customers, and VMware’s ongoing shift from perpetual to subscription licensing, which unlocks a more predictable, higher-margin revenue stream. The margin driver is software mix: net income margins are modeled expanding from the current 52.7% quarterly figure toward 53% at the mid-case, consistent with software gross margins, Kirsten Spears confirmed at 93% in Q1.

The upside case on the extended 10/31/34 horizon targets approximately $2,095, implying a 21% IRR, if AI revenue scales beyond the $100 billion 2027 target and software ARR growth sustains above 20% annually. The primary downside risk is customer concentration: if two or three XPU partnerships slow or delay simultaneously, the ~26% revenue CAGR assumption breaks down quickly.

The Street mean target is approximately $475. Per TIKR Street Targets as of May 7, 2026, the analyst rating breakdown is 36 Buys, 7 Outperforms, 3 Holds, and 4 No Opinions, with no Underperforms or Sells. That consensus implies around 15% upside from current levels, a more conservative near-term view than the TIKR mid-case, reflecting the market’s uncertainty about the OpenAI situation and broader AI capex sustainability.

Broadcom’s capital return program adds context. In Q1, the company returned $10.9 billion to shareholders through $7.8 billion in buybacks and $3.1 billion in dividends, and the board authorized an additional $10 billion repurchase program through December 2026. With $14.2 billion in cash and free cash flow of $8 billion in Q1 alone, Broadcom has significant capacity to continue buying back stock.

Conclusion

The number to watch at the June 3 Q2 earnings report is AI semiconductor revenue. Broadcom guided approximately $10.7 billion. If it meets or exceeds that, it confirms the OpenAI situation is isolated, and the five other customer ramps are carrying the thesis. If AI revenue misses, the $100 billion 2027 target comes into question. At $412.56, Broadcom remains one of the clearest structural beneficiaries of the AI infrastructure buildout. The OpenAI financing news adds real uncertainty to a story that had been running cleanly. It does not, on its own, change what the other five customer relationships say about where this business is headed.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Broadcom?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Broadcom, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Broadcom alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Broadcom on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!