Key Stats for Constellation Energy Stock

- 52-Week Range: $160.00 to $311.28 (approximate)

- Current Price: $311.28 TIKR

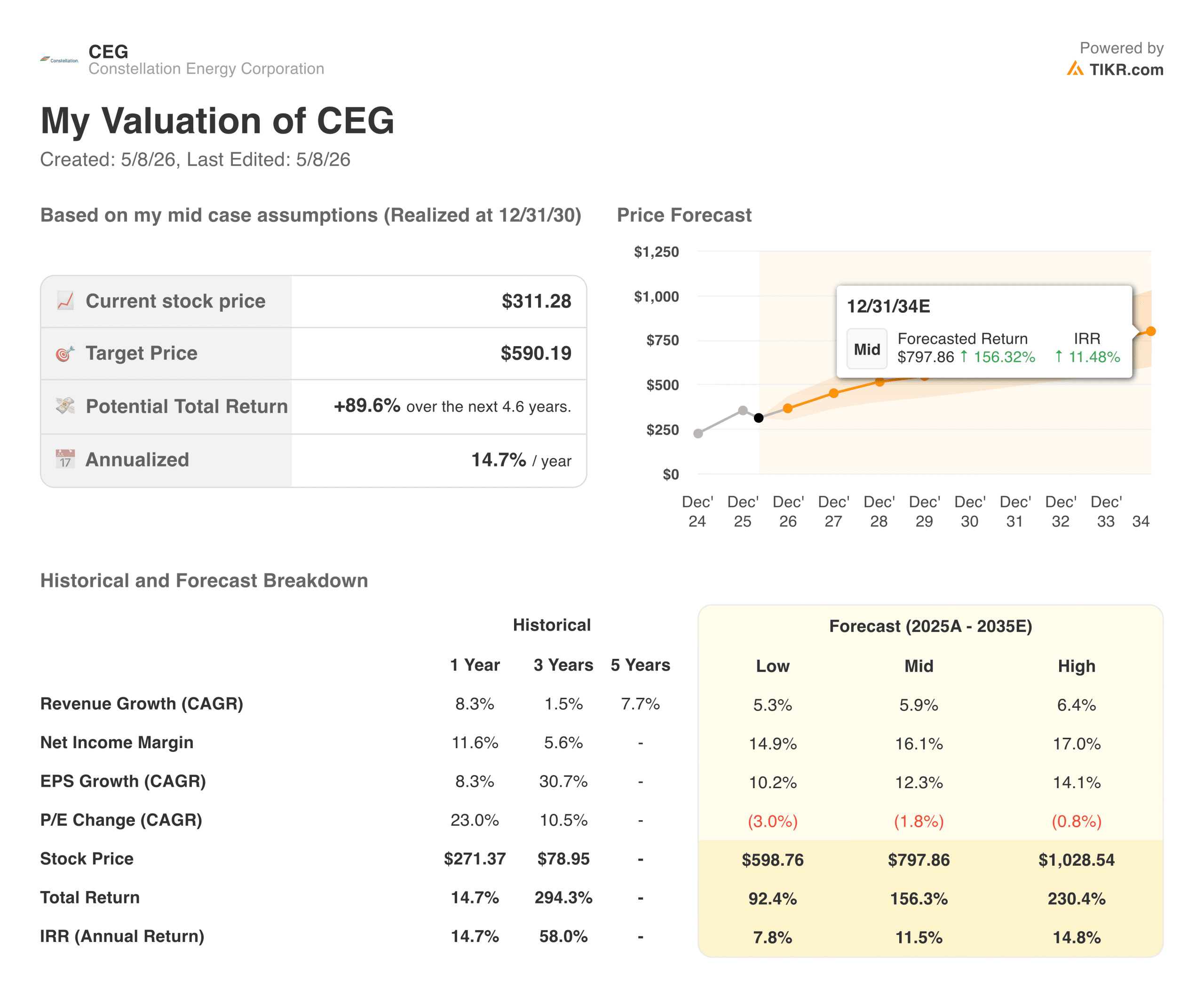

- Target Price (Mid): ~$590

- TIKR Annualized IRR (Mid): ~15% per year 2026

- EPS Guidance: $11.00 to $12.00

- Total Generation Capacity: ~55 GW

Value your favorite stocks like CEG with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Deal That Changed Everything

Constellation Energy (CEG) was already the largest nuclear operator in the United States before 2026. Then it closed the $16.4 billion acquisition of Calpine Corporation on January 7th, and the business became something different entirely.

The combined platform now controls roughly 55 gigawatts of generation capacity, pairing Constellation’s 22 gigawatts of nuclear with Calpine’s modern natural gas fleet and The Geysers, the largest geothermal complex in the world.

CEO Joe Dominguez described the result as a “one-stop shop for the global data economy,” and the framing is accurate in a way that matters for investors. What hyperscale technology companies need most is 24/7, carbon-free, reliable, and scalable power.

Nuclear provides the baseload. Natural gas provides the dispatchable backup. Very few companies can offer both, and Constellation is now the clearest example of one that can.

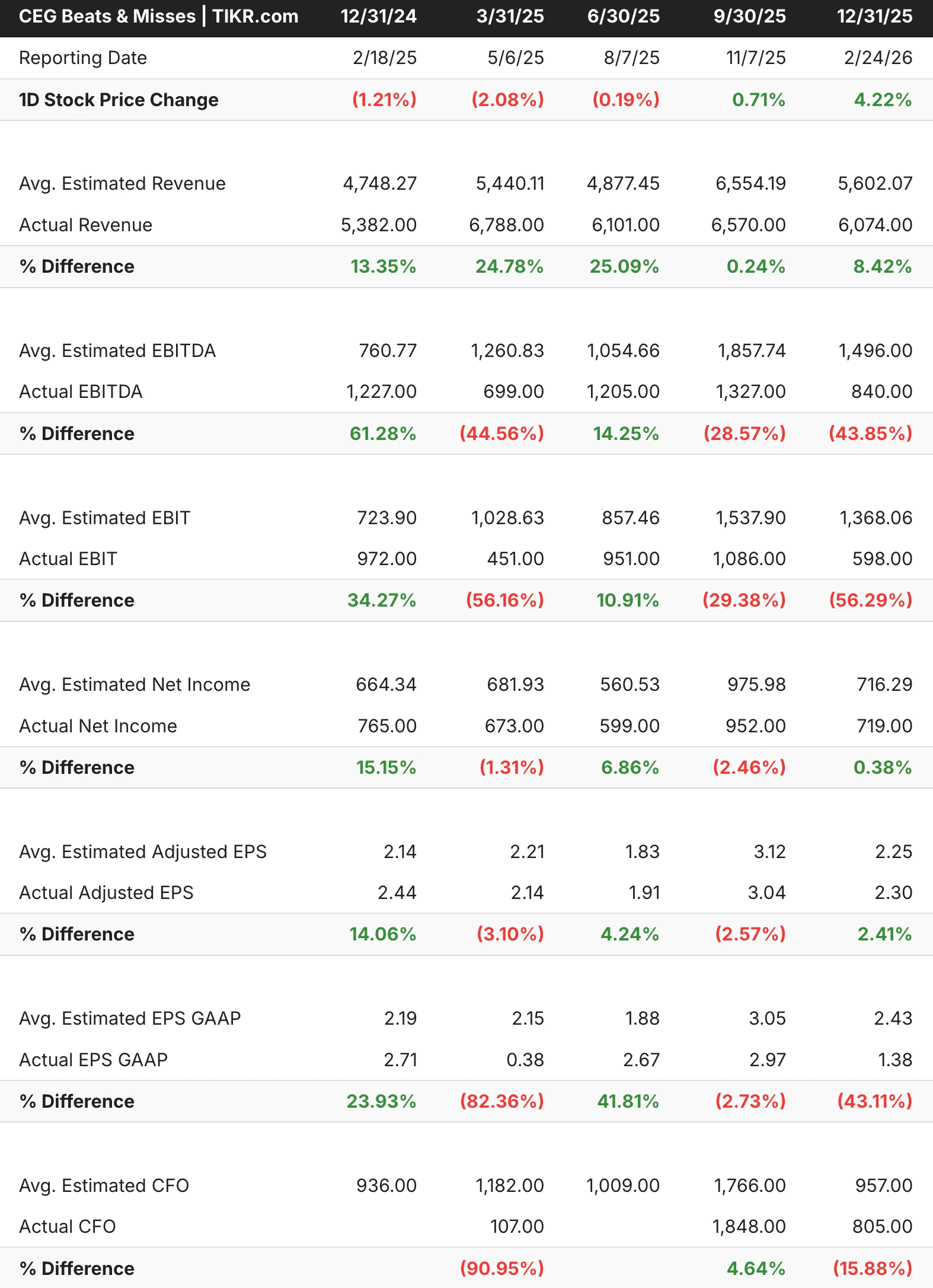

The beats-and-misses table reflects something important about this business that is easy to overlook: revenue consistently comes in well above analysts’ models. Three of the last five quarters showed revenue beats of 8% or more, with one quarter coming in nearly 25% above consensus. The EBITDA line is more volatile because power prices swing quarter to quarter, but the revenue consistency indicates the underlying demand for Constellation’s output is not in question.

See analysts’ growth forecasts and price targets for CEG stock (It’s free!) >>>

What the Revenue and Margin Chart Is Really Showing

The margin chart requires some context before drawing conclusions. Operating margins jumped from around 6% in 2023 to 18% in 2024, then compressed back to around 12% in 2025. That volatility is not a sign of business deterioration. It reflects how power markets work: wholesale electricity prices can move dramatically based on weather, gas prices, and grid conditions, and the timing of hedges and contracts creates apparent inconsistency in reported margins year to year.

What matters more than any single year’s operating margin is the underlying earnings power of the nuclear fleet, which operates at capacity factors near 95% and produces around 183 terawatt-hours of zero-emissions electricity annually. That output is increasingly contracted directly to technology companies at premium prices rather than sold into the spot market, which is gradually stabilizing the earnings profile in a way the headline margin numbers do not yet fully reflect.

Revenue has grown from $19.6 billion in 2021 to $25.5 billion in 2025, and with Calpine fully consolidated, the 2026 revenue base will be materially larger. Management has guided for 2026 adjusted EPS of $11.00 to $12.00, representing roughly 20% accretion from the acquisition.

Value CEG instantly (Free with TIKR) >>>

90% Upside in the Mid Case, With Real Execution Risk to Understand

TIKR’s model targets around $590 in the mid-case, implying a total return of roughly 90% over about 4.6 years, or about 15% annualized. The model assumes revenue growth of around 6% annually and net income margins expanding toward 16%, both of which are conservative relative to what the enlarged platform could deliver if data center power agreements continue to layer in.

What the Bulls Are Counting On

- The AI power demand story is structural, not cyclical. Data centers require 24/7 carbon-free power that wind and solar cannot reliably provide. Nuclear is the only scalable answer, and Constellation controls more nuclear capacity than any other private company in the country. Microsoft, Google, and other hyperscalers are signing long-term power purchase agreements at above-market rates specifically to secure this kind of power, and Constellation is the clearest beneficiary of that dynamic.

- Calpine adds a dimension that the pure nuclear story was missing. Technology companies do not just want clean power. They want firm power that stays on when the grid is stressed. Calpine’s natural gas fleet, particularly its roughly 23 gigawatts of combined cycle capacity, provides exactly that backup layer. The combined platform can now offer matched products that competitors simply cannot replicate at scale.

- The restart of the Crane Clean Energy Center adds long-term upside not reflected in the current numbers. The restart of the former Three Mile Island Unit 1 under a 20-year power purchase agreement with Microsoft represents incremental capacity coming online with contracted revenue already in place. That project moves from cost to earnings contributor as it progresses, creating a visible multi-year tailwind.

- The valuation has reset to a more reasonable level. At around $311, the stock is trading well below its 52-week high and at a meaningful discount to what TIKR’s mid-case model implies. The market has priced in execution risk around the Calpine integration and the March guidance miss, creating an entry point that did not exist six months ago.

What the Bears Are Watching

- The guidance miss in March was a real warning sign. When Constellation issued full-year 2026 EPS guidance with a midpoint of $11.50 against analyst consensus of around $11.73, the stock dropped more than 7% in a single session. Rising interest expenses from the Calpine financing and higher operating costs were the culprits. Those headwinds do not disappear quickly, and they represent genuine near-term margin pressure that the bull case needs to look through.

- Regulatory friction around data center co-location is a real constraint. The Federal Energy Regulatory Commission has been tightening rules around behind-the-meter arrangements that connect data centers directly to nuclear plants. Slower regulatory approval timelines mean the premium pricing story may take longer to fully materialize than the most optimistic scenarios assume.

- Integration risk is meaningful at this scale. Absorbing 23 gigawatts of generation capacity, 62 terawatt hours of retail load, and 2,500 employees while simultaneously restarting a nuclear plant is not a simple undertaking. Execution risk over the next 18 to 24 months is higher than it would be for a business in a steady state.

Should You Invest in Constellation Energy

Constellation is attempting something genuinely unusual: building a single platform that can serve as the primary power infrastructure for the AI economy while maintaining the operational discipline required to run the most complex generating assets in the country.

The bull case does not require the AI power demand story to be overhyped. It just requires Constellation to execute the Calpine integration, keep the nuclear fleet running at high capacity factors, and continue signing data center agreements at premium rates. All three of those things were true before the stock sold off, and none of them have materially changed.

The TIKR model’s mid-case target of around $590, against a current price of around $311, reflects genuine execution uncertainty. Whether that uncertainty is worth the implied upside is the question worth sitting with.

See analysts’ growth forecasts and price targets for CEG stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!